The air in the automotive and energy storage sectors is thick with anticipation. As an observer deeply embedded in this technological transition, I feel the collective pulse quickening around a single phrase: solid-state battery. What was once a distant promise on academic slides is now the central arena for global battery supremacy. The race for position has decisively begun, with nations and corporations staking their claims, driven by the belief that the solid-state battery holds the key to reshaping the future of electric mobility and energy infrastructure. Yet, amidst the soaring headlines and ambitious roadmaps, a sobering reality persists: the path to widespread, economical commercialization remains a multi-year journey. The consensus window for meaningful production and application appears to be 2026-2030, a period that will separate foundational research from transformative reality.

The fundamental appeal of the solid-state battery is rooted in its core architecture. By replacing the flammable liquid electrolyte in conventional lithium-ion cells with a solid counterpart, it directly attacks two critical limitations: safety and energy density. The risks of thermal runaway are drastically reduced. Simultaneously, the solid electrolyte can, in theory, enable the use of high-capacity lithium-metal anodes, unlocking a step-change in how much energy can be stored in a given volume or weight. The potential performance metrics are compelling, with energy densities projected to reach $$E_{SSB} = 400 – 900\ Wh/kg$$, significantly surpassing the plateau approaching $$E_{liquid} \approx 350\ Wh/kg$$ for advanced liquid lithium-ion batteries. This isn’t merely an incremental improvement; it represents a potential paradigm shift for vehicle range, design, and safety protocols.

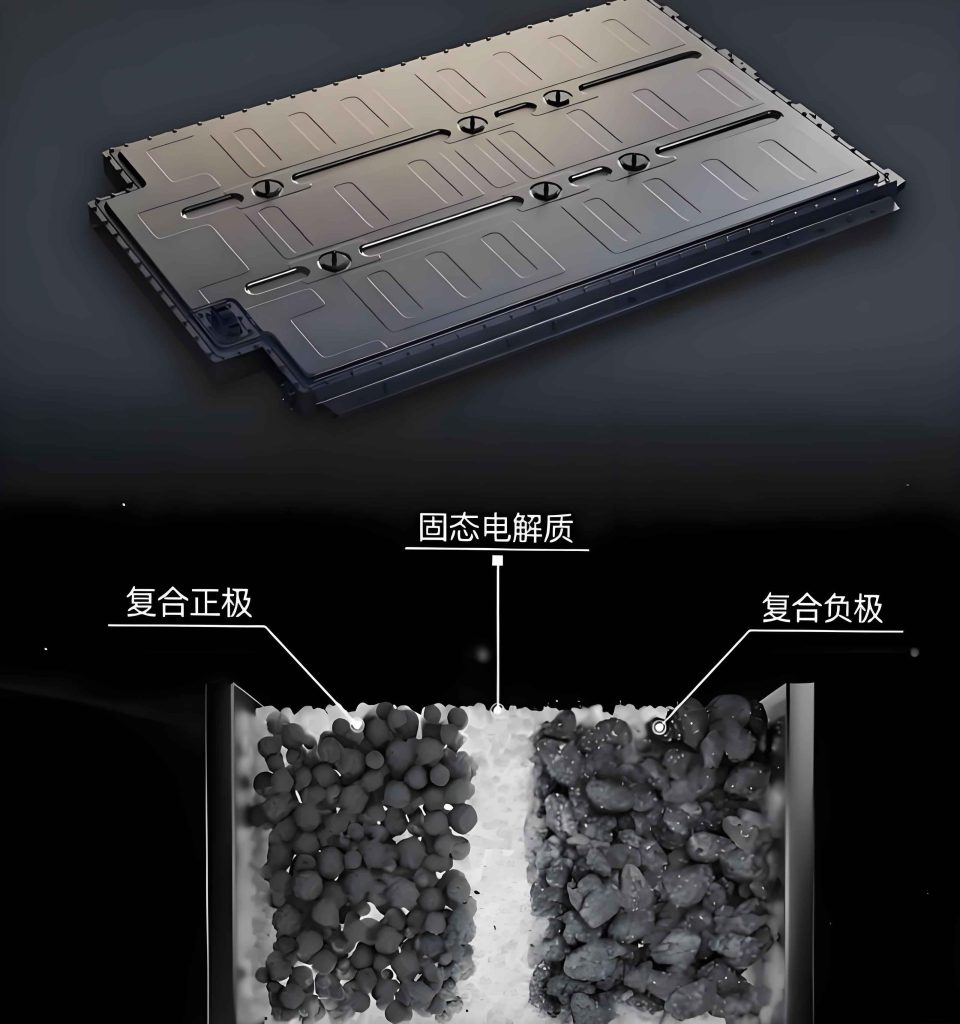

However, the term “solid-state battery” is not monolithic. The landscape is characterized by a parallel exploration of multiple technical pathways, primarily defined by the chemistry of the solid electrolyte. Each route presents a distinct set of trade-offs between ionic conductivity, mechanical stability, interfacial compatibility, and manufacturability.

| Electrolyte Pathway | Key Advantages | Primary Challenges | General Regional Focus |

|---|---|---|---|

| Polymer | Good flexibility, easier processing, decent interface contact. | Low ionic conductivity at room temperature, limited electrochemical stability window. | Europe, United States |

| Oxide | Excellent chemical and thermal stability, high mechanical strength. | Brittle nature, high interfacial resistance, challenging thin-film fabrication. | China |

| Sulfide | Very high ionic conductivity (rivaling liquids), good ductility. | Extreme sensitivity to moisture (generates toxic H₂S), poor stability against lithium metal, complex manufacturing. | Japan, South Korea |

| Halide | Promising stability against oxide cathodes, decent conductivity. | Emerging global research |

This diversity of approaches underscores a critical point: there is no universally agreed-upon “winner” for the solid-state battery formula. The development philosophy I see emerging is one of hybridization and pragmatism. Many players are investigating composite or multi-material electrolytes to balance these properties. For instance, combining a polymer’s flexibility with an oxide’s stability can create a more viable compromise for initial applications. The journey to the ideal solid-state battery is less a straight sprint and more a strategic traversal of a complex technological terrain.

The global timeline for the solid-state battery rollout is a mosaic of ambitious corporate and national strategies. While dates have shifted and should be viewed as optimistic targets, they reveal a clear clustering of expectations.

| Entity / Region | Announced Milestone (Semi-Solid) | Announced Milestone (Full Solid-State) |

|---|---|---|

| Japan (National Strategy) | N/A | Commercialization around 2030 |

| Various Chinese Automakers (e.g., GAC) | 2024-2025 (Vehicle integration) | 2026-2028 (Pilot/Initial production) |

| Toyota | N/A | Practical application 2027-2028; Mass production post-2030 |

| Nissan | N/A | Mass-market vehicle launch in 2028 |

| Korean Battery Makers (e.g., Samsung SDI) | N/A | Mass production targeted for 2027 |

| CATL | Already offering | Pilot production around 2027 |

| Academic Consensus (China) | Already initiating | Industrialization window: 2027-2030 |

This table illustrates a crucial industry dynamic: the near-term future belongs to the semi-solid-state battery. This intermediary technology, which reduces the liquid electrolyte content to around 5-10% but retains a separator, serves as a critical stepping stone. It delivers tangible, albeit incremental, improvements in safety and energy density—perhaps reaching $$E_{semi} = 350-500\ Wh/kg$$—using modified existing manufacturing lines. For the industry, it’s a vital learning platform, allowing for the refinement of new material interfaces and production processes while generating early market revenue. The year 2024 is widely seen as the starting point for meaningful semi-solid battery integration into production vehicles.

Yet, to believe the hype cycle uncritically would be a mistake. Between today’s promising prototypes and tomorrow’s affordable, reliable electric vehicles powered by solid-state batteries lie formidable barriers. From my analysis, the challenges coalesce into two primary categories: Fundamental Science & Engineering and Economics & Supply Chain.

1. The Core Scientific Hurdles: The solid-state battery is not just a swap of materials; it introduces a new set of physical and chemical problems. First, the interfaces between the solid electrolyte and the solid electrode materials are problematic. Unlike liquids, solids don’t conform perfectly, leading to high resistance at these boundaries that impedes ion flow and degrades performance. The quest is for a stable, low-resistance interface, which is exceptionally challenging when using a highly reactive lithium-metal anode. Second, dendrite formation—the growth of needle-like lithium structures—can still occur through microscopic defects in the solid electrolyte, leading to short circuits. While a solid electrolyte is more resistant than a porous separator, preventing dendrites over thousands of cycles is a major unsolved puzzle. Third, the ionic conductivity of most solid electrolytes, especially at room temperature, still lags behind advanced liquid electrolytes, affecting power and charging rates. These are not simple manufacturing tweaks; they require deep materials science innovations. The development status can be metaphorically represented on a maturity scale from 1 to 9. Many experts place current all-solid-state technology around a 4, with a level of 7 or 8 required for viable commercialization.

2. The Cost and Scale Mountain: Today, the cost premium for a solid-state battery, particularly one using lithium metal and advanced sulfides or oxides, is prohibitive. The equation is stark. Reports indicate a semi-solid battery pack can cost as much as an entire entry-level electric vehicle. The cost drivers are multifold:

- Material Costs: Precise, high-purity solid electrolyte powders (e.g., sulfides) are exponentially more expensive than liquid electrolyte salts and solvents. Lithium metal foil is costly and difficult to handle.

- Manufacturing: The entire production process differs. It often requires dense, thin ceramic sheets, controlled atmospheric rooms (especially for sulfides), and new stacking/assembly techniques. The capital expenditure for a giga-factory scale solid-state battery line is largely uncharted territory. Yield rates are a critical unknown.

- Supply Chain: A non-existent supply chain for key raw materials and production equipment must be built from the ground up.

We can model the necessary cost reduction as an exponential decay function, similar to what was achieved with liquid lithium-ion batteries:

$$C(t) = C_0 \times (1 – r)^t$$

Where \(C(t)\) is the cost at time \(t\), \(C_0\) is the current exorbitant cost, and \(r\) is the annual cost reduction rate. For the solid-state battery to become mainstream, \(r\) must be aggressive, driven by material innovation, process engineering, and, ultimately, massive scale. Analysts suggest that at scale, the cost of a solid-state battery could eventually fall below that of current lithium-ion batteries, but reaching that crossover point is the multi-year challenge.

The strategic implications are profound. The competitive landscape for the solid-state battery is a new front in the broader technology race. While certain regions have a head start in patent portfolios and specific material science (e.g., Japan with sulfides), the colossal scale of China’s battery material ecosystem and manufacturing prowess presents a formidable alternative pathway, primarily through oxide-based systems. The outcome is far from predetermined. The winning solid-state battery technology will likely be the one that optimally balances performance, safety, and cost—a trinity that is exceptionally difficult to achieve.

So, what is the realistic outlook? In my view, the evolution will be phased and coexistent. The lithium-ion battery, with continued incremental improvements, will dominate the market for at least the next 15-20 years. The semi-solid-state battery will capture niche, premium applications starting now, serving as the bridge technology. The true all-solid-state battery, the technology with the highest theoretical payoff, will likely see initial, very expensive applications in specialized fields (e.g., aerospace, premium automotive) towards the end of this decade, with a gradual trickle-down to mass-market automotive in the 2030s. The promise of the solid-state battery is undeniable—a safer, denser energy store that could alleviate many current consumer anxieties. But the path from laboratory breakthrough to a cost-competitive product in millions of vehicles is a marathon of engineering, requiring patience, immense investment, and a tolerance for iterative progress. The race is on, but the finish line for true, widespread transformation is still over the horizon.