The safety of portable energy storage has recently been thrust into the global spotlight. Widespread recalls of power banks due to cell safety risks, the revocation of 3C certifications for certain models, and the subsequent emergency “3C标识限制令” (3C marking restriction order) from civil aviation authorities have collectively amplified societal anxiety regarding the inherent safety limitations of liquid lithium-ion batteries. This growing concern acts as a potent catalyst, accelerating the development trajectory of the solid-state battery industry—a technology that promises a fundamental leap in safety by replacing flammable liquid electrolytes with solid counterparts. As the world undergoes a profound energy transition and industrial upgrading, the solid-state battery is widely recognized as a pivotal direction for next-generation power sources, attracting intense focus on its developmental progress. From my perspective, analyzing the current landscape, technological evolution, and future trajectory of China’s solid-state battery industry is not merely an academic exercise but a strategic necessity for maintaining and extending technological leadership in the new energy era.

The fundamental promise of the solid-state battery lies in its core architecture. By substituting the organic liquid electrolyte with a solid-state electrolyte—a material that is non-flammable and remains stable across a wide temperature range—it addresses the most critical vulnerability of contemporary batteries: thermal runaway. The advantages extend beyond safety. The use of a solid electrolyte enables the integration of high-capacity, high-voltage electrode materials, such as lithium metal anodes, that are incompatible or unstable with liquid systems, thereby unlocking significantly higher energy densities. This combination of enhanced safety and performance positions the solid-state battery as a transformative technology for electric vehicles (EVs), large-scale energy storage, and advanced consumer electronics. Recognizing this strategic importance, China has elevated the development of solid-state batteries to a national priority. Key policy documents, including the “New Energy Vehicle Industry Development Plan (2021–2035)” and the “High-Quality Development Action Plan for the New Energy Storage Manufacturing Industry,” explicitly designate solid-state battery technology as a critical frontier for focused research and industrial support. This top-down impetus has galvanized substantial domestic investment. Chinese companies are actively funding R&D and pilot production lines. Although global statistics are incomplete, the planned global capacity for solid-state batteries reportedly exceeds 800 GWh, with the vast majority of this capacity concentrated within China. This indicates not just ambition but a concerted effort to establish early-mover advantage in the next battery generation.

Current Status and the Pragmatic Path of Gradual Evolution

Despite the optimistic outlook and substantial investments, the path to a commercially dominant, pure solid-state battery is fraught with significant scientific and engineering hurdles. My analysis suggests that a direct, immediate leap to the ideal all-solid-state architecture is impractical. The core challenges are deeply rooted in material physics and interfacial chemistry.

The primary bottleneck lies in the solid-solid interface. Unlike the liquid electrolyte, which can permeate and maintain intimate contact with porous electrodes, the contact between a rigid solid electrolyte and a solid electrode is inherently poor. This leads to high interfacial resistance, severely limiting ionic conduction and power output. A related and equally critical issue is the instability at the anode interface when using lithium metal. While lithium metal is the “holy grail” anode material for energy density, it tends to form dendritic lithium枝晶 during cycling. In a liquid system, these dendrites can pierce the separator, causing a short circuit. In a solid-state system, they can fracture the brittle solid electrolyte, leading to contact loss, increased resistance, and eventually cell failure. Furthermore, the high cost of novel solid electrolyte materials and the complexities of scaling up their production with consistent quality present a formidable economic barrier.

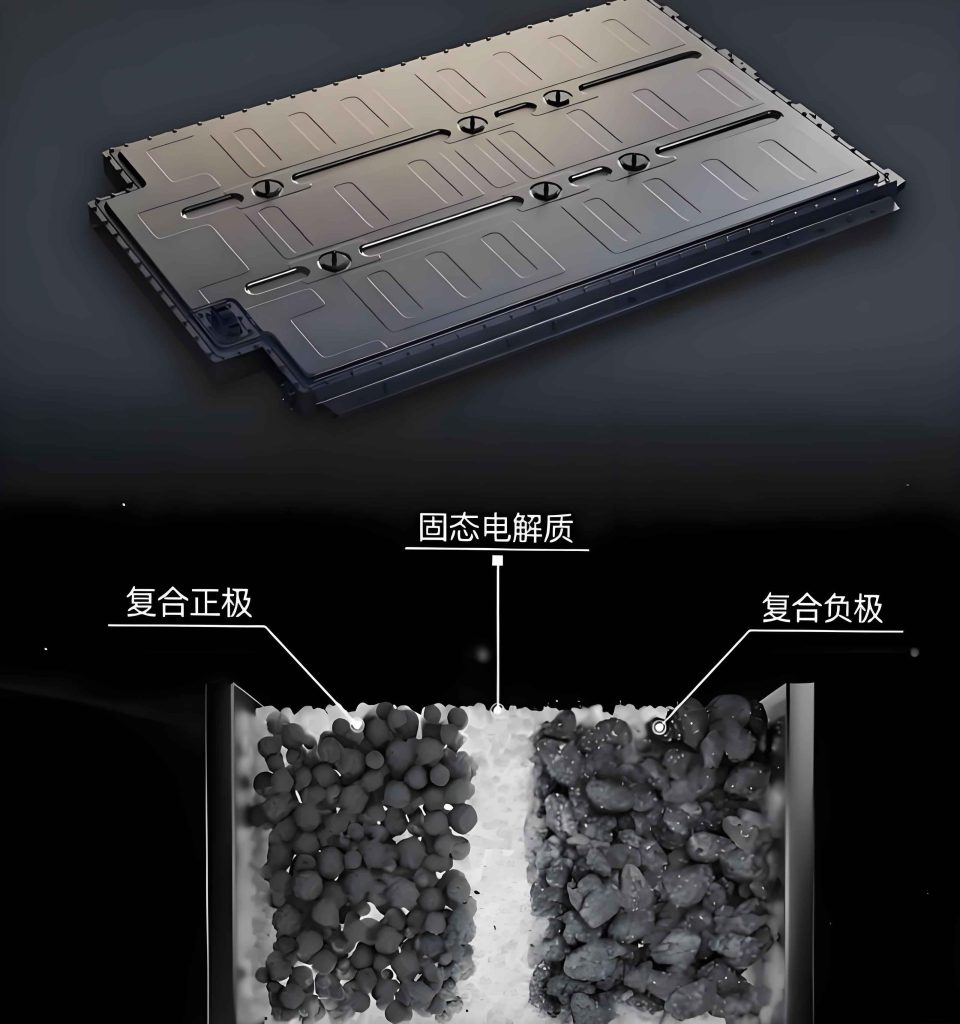

Confronted with these challenges, the industry has rationally adopted a phased, incremental strategy. Instead of targeting the perfect all-solid-state battery (ASSB) with zero liquid content, the focus has shifted to intermediate forms that blend solid and liquid components. This pragmatic approach serves as a crucial bridge technology.

- Semi-Solid-State Batteries: These contain a small percentage (typically 5-10% by mass) of liquid electrolyte. The liquid content significantly improves interfacial contact and ionic conductivity while still offering a substantial safety improvement over conventional liquid batteries due to the drastically reduced amount of flammable material.

- Quasi-Solid-State Batteries: These contain an even smaller liquid content (0-5%), pushing closer to the all-solid-state ideal.

The semi-solid-state battery, in particular, is poised for a prolonged transitional role. It effectively balances performance enhancement with cost control. On the performance side, it offers meaningful improvements in safety, energy density (alleviating range anxiety for EVs), and low-temperature operation—all of which are pressing market needs. Crucially, from a manufacturing perspective, semi-solid batteries can leverage the existing massive capital investment in liquid lithium-ion battery production. Approximately 70-90% of existing production equipment can be reused, with only new steps like solid electrolyte coating and vacuum liquid injection requiring addition. This reduces production line modification costs by an estimated 60%, making the technology economically viable in the near term. Therefore, I foresee a long-term coexistence where semi-solid batteries dominate the mainstream market for EVs and energy storage, while pure all-solid-state batteries gradually penetrate high-end, premium-performance segments. Industry forecasts, such as those from BloombergNEF, project that by 2035, semi-solid batteries could constitute around 70% of the global solid-state battery market. This establishes a “semi-solid mainstream, all-solid supplementary” technological ecosystem for decades to come.

China’s current industrial strength provides a formidable foundation for this transition, albeit with a critical weakness. The country is the undisputed global leader in the conventional lithium-ion battery supply chain. As shown in Table 1, China’s production share exceeds 90% for key materials like lithium iron phosphate (LFP) cathode, anode materials, separators, and electrolyte. In 2024, it produced an estimated 1,170 GWh of lithium-ion batteries, commanding about 76% of the global market, with exports valued at $61.1 billion.

| Material | 2024 Production | YoY Growth | Global Share |

|---|---|---|---|

| LFP Cathode | 2.397 million tons | 55.7% | >99% |

| Anode Material | 2.104 million tons | 22.7% | 98% |

| Separator | 214.5 billion m² | 23.5% | 91.3% |

| Electrolyte | 1.493 million tons | 41.1% | 91.4% |

This dominance extends to technological advancements. In cathodes, LFP and high-nickel NCM (Nickel Cobalt Manganese) are driving innovation. In anodes, synthetic graphite technology is world-leading, and silicon-based anodes are accelerating towards commercialization. In separators, wet-process technology dominates, with advanced coated and composite separators already being used in semi-solid-state battery prototypes from leading firms. In soft-pack packaging, aluminum laminate film is achieving import substitution. However, the core enabler of the solid-state battery revolution—the solid electrolyte itself—remains an area where China’s progress is relatively slower and more fragmented. While Chinese companies and research institutions are exploring all four major solid electrolyte families (oxide, sulfide, polymer, and halide), the strategic focus in Japan and South Korea is sharply concentrated on the sulfide route for all-solid-state batteries. China’s approach is more diversified and transitional, with most companies focusing on the lower-barrier oxide and polymer routes for semi-solid applications. The planned mass-production timelines for all-solid-state batteries from leading Chinese battery giants generally lag behind their Japanese and Korean counterparts by a few years, indicating a technology gap that needs to be closed.

Technological Trajectory and Evolving Material Ecosystem

The evolution of the solid-state battery is not an isolated event but a systemic shift that will redefine the entire battery material supply chain. Based on current R&D trends, a consensus is forming on the direction for most core materials, while the battle for the optimal solid electrolyte continues.

Cathode and Anode Evolution

In the short to medium term, cathode development will involve enhancing existing systems. For high-nickel NCM cathodes, single-crystal morphology, oxide coating, and metal doping are key strategies to improve structural stability and energy density. The equation for gravimetric energy density highlights the importance of capacity and voltage:

$$ E_{grav} = \frac{C_{cathode} \times V_{avg}}{1 + \frac{m_{anode} + m_{inactive}}{m_{cathode}}}} $$

where \( E_{grav} \) is gravimetric energy density, \( C_{cathode} \) is the cathode capacity, \( V_{avg} \) is the average discharge voltage, and the denominator represents the mass ratio of all other components to the cathode. Increasing \( C_{cathode} \) and \( V_{avg} \) is crucial. This drives the development of Lithium-Rich Manganese-Based (LRM) cathodes, which offer both higher specific capacity (>250 mAh/g) and higher operating voltages than conventional NCM. Their manganese-rich composition also reduces cost and improves safety. Chinese material suppliers have begun small-scale shipments of LRM materials.

For anodes, graphite is approaching its theoretical limit (~372 mAh/g). The next step is silicon-based anodes (Si-C, Si-O), with theoretical capacities an order of magnitude higher:

$$ C_{Si} (Li_{22}Si_5) \approx 4200 \, mAh/g \quad vs. \quad C_{graphite} (LiC_6) \approx 372 \, mAh/g $$

These will be essential for semi- and quasi-solid-state batteries to reach higher energy densities. The ultimate goal, however, is the lithium metal anode, which has a theoretical capacity of 3,860 mAh/g and can act as its own current collector, simplifying design. The challenge is formulated by the instability of the solid electrolyte interphase (SEI) and dendrite growth. The critical current density \( J_{crit} \) before dendrite initiation is a key parameter that solid electrolytes must maximize:

$$ J_{crit} \propto \frac{\mu \sigma}{E} $$

where \( \mu \) is the shear modulus, \( \sigma \) is the ionic conductivity, and \( E \) is the Young’s modulus of the electrolyte. This underscores the need for a solid electrolyte that is both highly conductive and mechanically robust.

The Solid Electrolyte Conundrum

The choice of solid electrolyte is the most critical and uncertain decision in solid-state battery development. Each of the four primary families presents a distinct set of trade-offs, as summarized in Table 2. China’s industry is currently dominated by polymer and oxide electrolytes for semi-solid applications, but the long-term race is open.

| Route | Ionic Conductivity (S/cm) | Key Advantages | Key Challenges | Development Stage in China |

|---|---|---|---|---|

| Sulfide | $10^{-4}$ – $10^{-2}$ | Highest conductivity, good rate performance, high energy density potential. | Extreme sensitivity to moisture (H₂S generation), poor interfacial stability with oxides, high cost. | Prototype validation, material development. |

| Oxide | $10^{-5}$ – $10^{-3}$ | High voltage stability, good safety, high theoretical capacity. | Brittle, poor solid-solid contact, high grain boundary resistance. | Leading route for semi-solid development. |

| Polymer | $10^{-7}$ – $10^{-5}$ | Excellent flexibility, good interfacial contact, easy processing, long cycle life. | Low conductivity (requires heating), narrow electrochemical window. | Leading route for semi-solid development. |

| Halide | $10^{-5}$ – $10^{-3}$ | Good voltage/thermal stability, compatible with oxide cathodes. | Reduction instability with Li metal, moderate conductivity. | Early experimental stage. |

The sulfide route, championed by Japanese firms, offers the highest ionic conductivity—a parameter vital for achieving power performance comparable to liquid batteries. The conductivity \( \sigma \) is given by the Nernst-Einstein relation:

$$ \sigma = n z q \mu $$

where \( n \) is the charge carrier density, \( z \) is the charge number, \( q \) is the elementary charge, and \( \mu \) is the carrier mobility. Sulfides excel in creating high \( n \) and \( \mu \). However, their sensitivity to moisture and complex interface issues are major hurdles. The oxide route is more stable but suffers from high interfacial resistance. The polymer route is process-friendly but thermally limited. The halide route is a promising newcomer but less mature. I observe that over 60% of Chinese enterprises are hedging their bets by pursuing 2-3 different technical routes simultaneously, reflecting the high uncertainty.

Disruptive Innovations and Supporting Material Shifts

Beyond incremental improvements, truly disruptive concepts are emerging. One notable example is the “anode-less” or “in-situ formed anode” technology. This approach eliminates the pre-fabricated anode material (graphite or silicon). Instead, lithium ions are plated directly onto a bare current collector during the first charge, creating a lithium metal anode in situ. This dramatically simplifies manufacturing and increases energy density by removing inert anode material mass. It also aims to create a more uniform lithium deposition, mitigating dendrite growth. This innovation could accelerate the leap from silicon-based anodes to practical lithium metal anodes.

The supporting material ecosystem is also adapting. For separators, their role is evolving rather than disappearing. In semi-solid batteries, they remain essential. A significant trend is the development of “sulfide-coated separators.” These composite membranes, created by coating traditional polyolefin separators with a thin layer of sulfide solid electrolyte particles, represent a clever transitional product. They improve safety by reducing liquid electrolyte content and serve as a practical testbed for sulfide material processing and interface engineering, de-risking the future path to all-solid-state batteries.

Another critical shift is in cell packaging. Leading consumer electronics companies are moving from aluminum laminate film (soft-pack) to steel-can (prismatic/hard-case) designs for their latest devices. This aligns with new regulations emphasizing replaceability and, more importantly, prepares the supply chain for solid-state batteries. Steel cans offer superior hermeticity, which is crucial for protecting moisture-sensitive sulfide electrolytes during long-term operation. They also provide better mechanical support to contain the volume expansion of next-generation anodes like silicon. This strategic move by downstream giants is a strong signal guiding upstream material and cell design choices towards formats compatible with the future solid-state battery paradigm.

Strategic Recommendations for Industrial Development

Given the complex landscape, a strategic and multi-pronged approach is essential for China to solidify its leadership in the next generation of battery technology. My analysis leads to the following recommendations, formulated from the perspective of an industry strategist.

1. Leverage the Liquid Battery Legacy While Aggressively Pioneering the Solid-State Future. It is crucial to recognize that conventional liquid lithium-ion batteries will remain the workhorse of energy storage for at least the next 15-20 years due to their unrivaled cost-performance maturity. The existing material supply chain represents a colossal strategic asset. The focus should be on dual-track advancement: First, continue to optimize and export the current liquid battery ecosystem, advancing high-nickel single-crystal cathodes, silicon-carbon anodes, ultra-thin high-strength separators, and high-performance aluminum laminate film. Second, use the profits and technological learnings from this dominant position to fund aggressive R&D into solid-state battery leapfrog technologies. The window for liquid battery dominance is finite but still wide enough to finance the future.

2. Build a National Solid-State Electrolyte Technology Consortium and Talent Pipeline. The fragmented, parallel, and sometimes redundant R&D efforts across companies and institutes create inefficiencies. The high technical barriers and route uncertainty demand a coordinated national effort. I propose the establishment of a “National Solid-State Electrolyte Technology Innovation Alliance.” This alliance would integrate upstream material scientists, mid-stream battery engineers, and downstream application OEMs (e.g., EV manufacturers). Its mandate would be to:

- Share fundamental research data on interface degradation mechanisms, ion transport modeling, and material stability.

- Coordinate the standardization of testing protocols for solid-state battery cells and materials.

- Pool resources for expensive, shared infrastructure like dry room pilot manufacturing lines for sulfide electrolyte processing.

- Jointly tackle grand challenges, such as stabilizing the lithium metal/sulfide electrolyte interface, which can be described by the competing kinetics of Li plating versus SEI formation.

Simultaneously, a dedicated talent strategy is needed. This involves attracting global experts, fostering cross-disciplinary programs in materials science, electrochemistry, and mechanical engineering, and creating clear career pathways for researchers within the solid-state battery ecosystem.

3. Secure Critical Resources and Forge Deep Vertical Integration. The solid-state battery of the future, whether based on LRM cathodes, lithium metal anodes, or sulfide electrolytes, will intensify dependence on specific critical minerals like lithium, cobalt, nickel, and manganese. Geopolitical moves to destabilize supply chains for these materials pose a direct threat. Strategic upstream investment, through partnerships or direct ownership in global mining assets, is non-negotiable for ensuring supply security and cost stability. Furthermore, companies should deepen vertical integration. Battery cell manufacturers could partner with or invest in solid electrolyte producers. Material companies should form joint development agreements (JDAs) with cell makers to co-develop application-specific materials. Such integration reduces transaction costs, accelerates feedback loops, and builds more resilient and competitive industrial clusters specifically tailored for the solid-state battery age.

In conclusion, the transition to the solid-state battery is inevitable but will be gradual and iterative. China possesses the unparalleled scale of its existing battery industry, strong policy support, and vibrant innovation ecosystem to lead this transition. The key to success lies in a balanced strategy: ruthlessly optimizing the present liquid-based technology to fund and de-risk the future, fostering unprecedented collaboration to overcome the core scientific hurdles of solid electrolytes, and strategically securing the entire value chain from mine to cell. By executing this strategy, China can transform its current manufacturing supremacy into enduring technological leadership in the era of the solid-state battery.