In my extensive experience analyzing the energy storage and electric vehicle industries, I have witnessed a rapid transformation driven by technological innovation and market dynamics. The heart of this evolution lies in battery technology, where the quest for higher energy density, safety, and cost-effectiveness continues to shape the future. Among the myriad of advancements, solid-state batteries have emerged as a pivotal frontier, promising to address the limitations of current lithium-ion systems. As I delve into this topic, I will explore the current state of the battery industry, the promise and challenges of solid-state batteries, and the broader implications for global energy storage. Throughout this discussion, I will emphasize the critical role of solid-state batteries, a term that will recur as we navigate the complexities of this field.

The global battery market, particularly for electric vehicles, has seen exponential growth over the past decade. From my perspective, this growth is fueled by policy support, environmental concerns, and technological breakthroughs. However, it is accompanied by significant challenges such as产能过剩 (overcapacity) and resource constraints. To contextualize this, let me present a table summarizing key metrics in the动力电池 (power battery) industry:

| Year | Global Lithium Power Battery Shipments (GWh) | China’s Share (%) | Average Capacity Utilization (%) |

|---|---|---|---|

| 2011 | 1.08 | ~30 | ~60 |

| 2017 | 62.35 | >60 | ~40 |

| 2020 (Projected) | ~200 | >65 | ~50 |

As evident, China has become a dominant player, but the declining capacity utilization indicates structural issues. In my view, this stems from fragmented investments and a focus on low-end technologies, rather than core innovations. The competition is intensifying, with Japan, South Korea, and Europe vying for leadership, especially in next-generation technologies like solid-state batteries. I believe that solid-state batteries represent a paradigm shift, but before delving deeper, let’s examine the technical foundations.

Current mainstream batteries, primarily lithium-ion based, rely on liquid electrolytes. Their energy density can be approximated by the formula: $$E_d = \frac{C \times V}{m}$$ where \(E_d\) is the energy density in Wh/kg, \(C\) is the capacity in Ah, \(V\) is the voltage, and \(m\) is the mass. For typical三元 (ternary) batteries, \(E_d\) ranges from 200-300 Wh/kg. However, safety concerns and limited improvement trajectories have spurred research into solid-state batteries. A solid-state battery replaces the liquid electrolyte with a solid medium, often using lithium metal as the anode. This can theoretically boost energy density. I estimate that solid-state batteries could achieve: $$E_d^{solid} = \frac{Q_{Li} \times \phi}{V_{cell}}$$ where \(Q_{Li}\) is the lithium capacity, \(\phi\) is the efficiency factor, and \(V_{cell}\) is the cell voltage. With lithium metal anodes, \(E_d^{solid}\) may exceed 500 Wh/kg.

The potential of solid-state batteries is immense, but numerous bottlenecks persist. From my analysis, key technical hurdles include ionic conductivity of solid electrolytes, interfacial stability, and manufacturing scalability. To illustrate, the ionic conductivity \(\sigma\) of a solid electrolyte often follows the Arrhenius equation: $$\sigma = \sigma_0 \exp\left(-\frac{E_a}{kT}\right)$$ where \(\sigma_0\) is a pre-exponential factor, \(E_a\) is the activation energy, \(k\) is Boltzmann’s constant, and \(T\) is temperature. Current solid electrolytes have \(\sigma\) values orders of magnitude lower than liquids, limiting charge/discharge rates. Additionally, the solid-solid interface between electrolyte and electrodes poses challenges in maintaining contact and preventing dendrite formation. I have compiled a table comparing different battery technologies:

| Battery Type | Energy Density (Wh/kg) | Cycle Life | Safety | Cost ($/kWh) | Status |

|---|---|---|---|---|---|

| Lithium-ion (Liquid Electrolyte) | 200-300 | 1000-2000 | Moderate | 100-150 | Commercial |

| Solid-State Battery (First Layer) | 250-350 | 500-1000 | High | 200-300 | R&D/Pilot |

| Solid-State Battery (Second Layer) | >500 | >1000 | Very High | 150-200 (Projected) | Experimental |

| Lithium-Sulfur | 400-600 | 500-800 | Low | 80-120 (Projected) | R&D |

In my opinion, the distinction between “first layer” and “second layer” solid-state batteries is crucial. The first layer refers to replacing only the electrolyte in existing designs, which improves safety but offers limited gains. The second layer involves a full material overhaul, such as using lithium-sulfur or lithium-metal anodes. I contend that true solid-state batteries belong to the second layer, but they are at least a decade away from commercialization. This aligns with industry sentiments that innovation must be incremental yet bold.

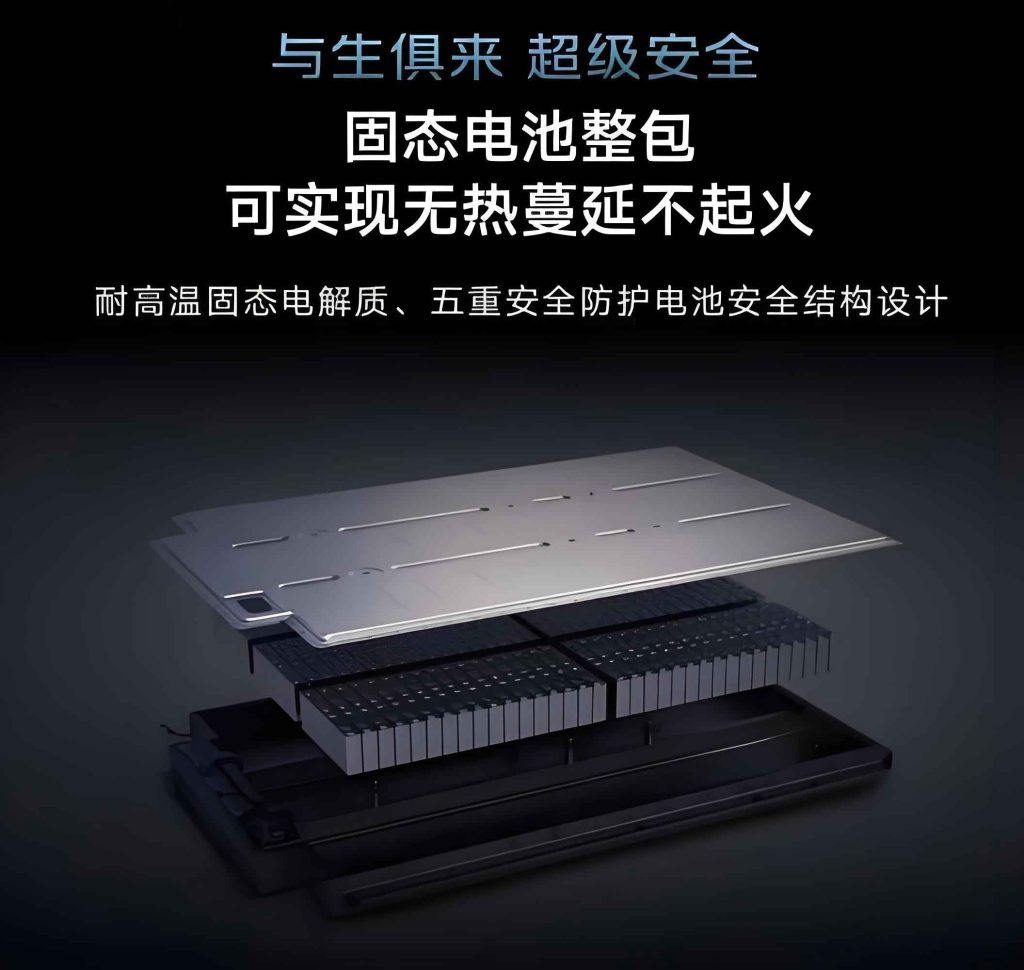

The image above visually represents the structure of a solid-state battery, highlighting its compact and safe design. As I reflect on this, the promise of solid-state batteries extends beyond performance. They could mitigate resource risks associated with materials like cobalt and nickel. Speaking of resources, the global distribution of key电池 materials is highly concentrated, posing supply chain vulnerabilities. From my research, here’s a summary:

| Material | Top Producing Countries (Share %) | Global Reserves (Million Tons) | China’s Dependence (%) |

|---|---|---|---|

| Lithium | Chile (40%), Australia (30%), China (15%) | 17 | ~60 |

| Cobalt | DR Congo (70%), Russia (4%), Australia (4%) | 7 | >90 |

| Nickel | Indonesia (25%), Philippines (15%), Russia (10%) | 94 | >80 |

I worry that this oligopoly could hinder the growth of电池 industries, especially as demand surges. Solid-state batteries, by potentially reducing reliance on cobalt through new chemistries, offer a path forward. For instance, lithium-metal anodes in solid-state batteries may use less cobalt or none at all. The cost dynamics can be modeled as: $$C_{total} = C_{mat} + C_{manuf} + C_{R&D}$$ where \(C_{mat}\) is material cost, \(C_{manuf}\) is manufacturing cost, and \(C_{R&D}\) is research amortization. For solid-state batteries, \(C_{mat}\) might decrease due to simpler materials, but \(C_{manuf}\) remains high due to nascent processes. I project that with scale, costs could drop to: $$C_{solid} \approx \frac{1}{3} C_{liq}$$ where \(C_{liq}\) is current lithium-ion battery cost, aligning with some industry targets of under $100/kWh.

Innovation in solid-state batteries is not occurring in isolation. Other emerging technologies, such as lithium-air and sodium-ion batteries, are also being explored. However, in my assessment, solid-state batteries have garnered the most attention due to their compatibility with existing manufacturing frameworks. The race for dominance is global, with significant investments from companies in China, Japan, Germany, and the United States. I have observed that collaboration between academia and industry is vital, yet often lacking. To quantify progress, consider the research output index \(I\) for solid-state batteries: $$I = \frac{N_{patents} \times \alpha}{T_{delay}}$$ where \(N_{patents}\) is the number of patents filed, \(\alpha\) is an impact factor, and \(T_{delay}\) is the time to commercialization. Currently, \(I\) is rising but remains below thresholds for mass adoption.

From a first-person perspective, I see the battery industry at a crossroads. The push for solid-state batteries is emblematic of broader trends in energy storage. However, challenges like investment虚化 (virtualization) and产能过剩 (overcapacity) must be addressed. I advocate for a balanced approach: fostering基础 (basic) research while aligning it with market needs. The公式 for success might be: $$S = \beta \times I_{tech} \times \gamma_{policy}$$ where \(S\) is success probability, \(\beta\) is a scaling factor, \(I_{tech}\) is technological innovation index, and \(\gamma_{policy}\) is policy support efficacy. For solid-state batteries, both \(I_{tech}\) and \(\gamma_{policy}\) need enhancement.

Looking ahead, the timeline for solid-state battery adoption is uncertain. Some predict commercialization by 2030, but I caution that technical hurdles are substantial. The charging time \(t_{charge}\) for a solid-state battery could be reduced significantly, as per: $$t_{charge} = \frac{E}{P_{charge}} \times \eta$$ where \(E\) is energy capacity, \(P_{charge}\) is charging power, and \(\eta\) is efficiency. With solid electrolytes enabling faster ion transport, \(t_{charge}\) might approach 10 minutes for a full charge, a game-changer for electric vehicles. Nevertheless, durability issues persist, as cycle life \(N_{cycle}\) often degrades with high current densities: $$N_{cycle} = N_0 \exp\left(-\frac{J}{J_0}\right)$$ where \(N_0\) is initial cycle life, \(J\) is current density, and \(J_0\) is a critical threshold.

In conclusion, solid-state batteries represent a transformative technology with the potential to redefine energy storage. As I have outlined, their advantages in energy density, safety, and resource efficiency are compelling, but the path to widespread use is fraught with technical and economic barriers. The industry must prioritize core innovations, avoid low-end产能扩张 (capacity expansion), and foster international collaboration. I am optimistic that with sustained effort, solid-state batteries will eventually overcome these challenges, paving the way for a sustainable energy future. The journey is complex, but the destination—a world powered by advanced, safe, and efficient batteries—is worth the pursuit.

To further elaborate, let’s consider the environmental impact of battery production. Solid-state batteries could reduce the carbon footprint through longer lifespans and fewer hazardous materials. The lifecycle emissions \(E_{LC}\) can be expressed as: $$E_{LC} = E_{prod} + E_{use} + E_{EOL}$$ where \(E_{prod}\) is production emissions, \(E_{use}\) is use-phase emissions, and \(E_{EOL}\) is end-of-life emissions. For solid-state batteries, \(E_{prod}\) might be higher initially due to energy-intensive manufacturing, but \(E_{use}\) could be lower due to higher efficiency, and \(E_{EOL}\) might be reduced through better recyclability. I estimate that over a 10-year period, solid-state batteries could cut \(E_{LC}\) by up to 30% compared to conventional lithium-ion batteries.

Moreover, the integration of solid-state batteries with renewable energy systems is a promising avenue. In grid storage applications, the response time \(\tau\) of a battery is critical: $$\tau = \frac{R_{int} \times C}{V}$$ where \(R_{int}\) is internal resistance, \(C\) is capacitance, and \(V\) is voltage. Solid-state batteries typically exhibit lower \(R_{int}\) due to better ion conduction, leading to faster \(\tau\). This makes them ideal for smoothing intermittent renewable sources like solar and wind. I envision a future where solid-state battery farms provide stable, high-power backup, enhancing grid resilience.

From an economic standpoint, the market for solid-state batteries is poised for growth. Projections suggest a compound annual growth rate (CAGR) of over 50% in the next decade. The revenue \(R\) can be modeled as: $$R = P \times Q \times \delta$$ where \(P\) is price per kWh, \(Q\) is quantity sold, and \(\delta\) is a market penetration factor. As technology matures, \(P\) is expected to decline, while \(Q\) and \(\delta\) increase. I predict that by 2040, solid-state batteries could capture more than 40% of the global battery market, driven by automotive and stationary storage demands.

In my final thoughts, I emphasize that the development of solid-state batteries is not just a technical endeavor but a strategic imperative. Nations and companies investing in this technology are positioning themselves for leadership in the coming energy era. As I have repeatedly highlighted, solid-state batteries hold the key to unlocking higher performance and sustainability. However, success requires patience, collaboration, and a relentless focus on innovation. The road ahead is long, but with each breakthrough in solid-state battery research, we move closer to a brighter, cleaner energy landscape.