As a leading analyst in the energy storage sector, I have been closely monitoring the rapid evolution of battery technologies. Among these, the solid-state battery stands out as a transformative solution, poised to redefine energy storage across multiple industries. In this article, I will delve into the current market landscape, technological pathways, and future trajectories of solid-state batteries, drawing from extensive research and data analysis. The transition from liquid electrolytes to solid-state systems is not merely an incremental improvement but a paradigm shift that promises enhanced safety, higher energy density, and broader application scopes. With global interest surging, the race to commercialize solid-state batteries is intensifying, and understanding the dynamics at play is crucial for stakeholders.

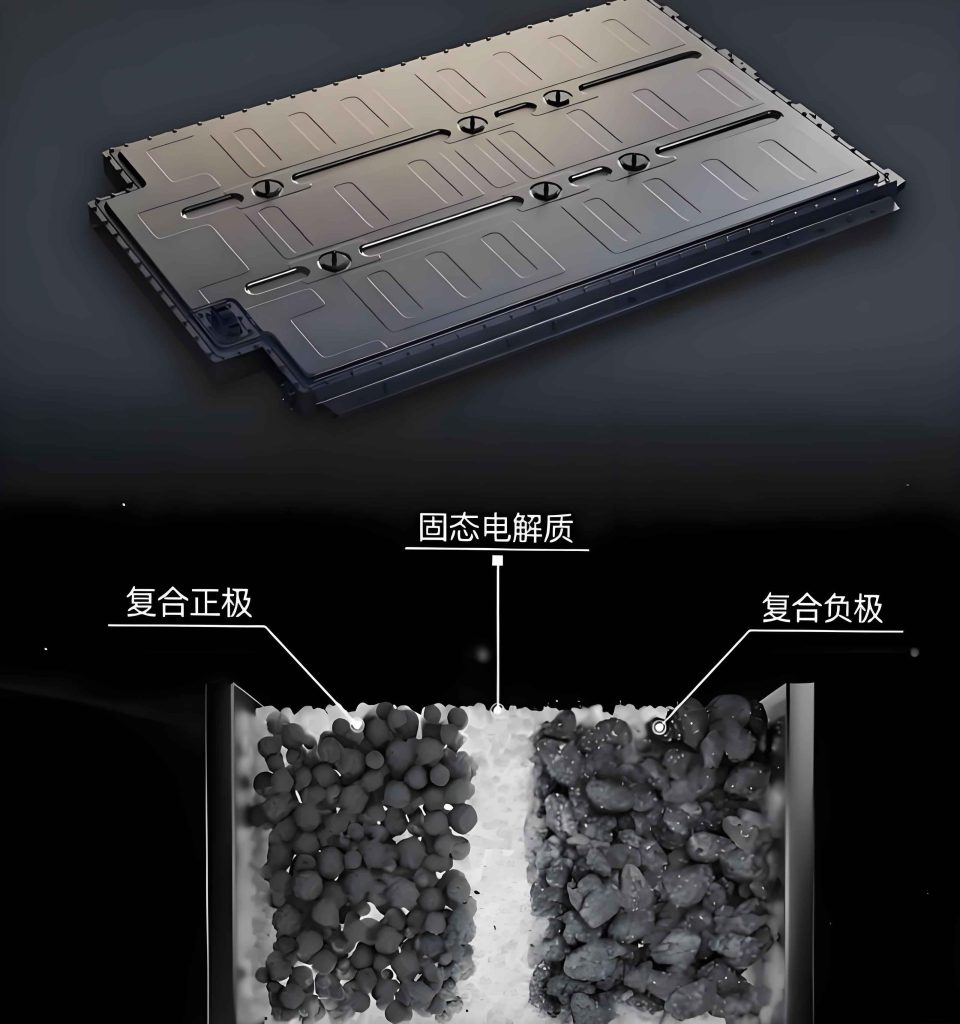

The solid-state battery represents a significant departure from conventional lithium-ion batteries that rely on liquid or gel electrolytes. By employing solid electrolytes, these batteries mitigate risks such as leakage, thermal runaway, and dendrite formation, which have long plagued traditional systems. The core advantages can be summarized through key performance metrics. For instance, energy density, a critical parameter for electric vehicles and portable electronics, is expected to see substantial gains. We can express the theoretical energy density of a solid-state battery using the formula: $$ E_{ss} = \frac{Q \cdot V}{\rho} $$ where \( E_{ss} \) is the energy density, \( Q \) is the charge capacity, \( V \) is the voltage, and \( \rho \) is the mass density. Compared to liquid counterparts, solid-state batteries often achieve higher \( V \) due to stable interfaces, leading to \( E_{ss} \) values potentially exceeding 500 Wh/kg, a milestone that liquid lithium-ion batteries struggle to reach.

To illustrate the fundamental differences, I have compiled a comparative table highlighting key characteristics of solid-state batteries versus traditional liquid lithium-ion batteries. This comparison underscores why the solid-state battery is garnering such attention.

| Feature | Liquid Lithium-Ion Battery | Solid-State Battery |

|---|---|---|

| Electrolyte State | Liquid or gel | Solid (e.g., ceramics, polymers) |

| Energy Density (Typical) | 200-300 Wh/kg | 300-500+ Wh/kg (projected) |

| Safety | Moderate (risk of leakage, fire) | High (reduced flammability) |

| Cycle Life | 500-1000 cycles | 1000+ cycles (expected) |

| Operating Temperature Range | -20°C to 60°C | -40°C to 100°C (potential) |

| Cost (Current) | Low to moderate | High (decreasing with scale) |

The technological pathways for solid-state batteries are diverse, primarily categorized into semi-solid and all-solid configurations. Semi-solid batteries, which incorporate some liquid components, serve as an intermediate step, offering easier manufacturability while improving safety. In contrast, all-solid batteries eliminate liquids entirely, aiming for maximum performance. The ionic conductivity \( \sigma \) of solid electrolytes is a critical factor, often described by the Arrhenius equation: $$ \sigma = A \exp\left(-\frac{E_a}{kT}\right) $$ where \( A \) is a pre-exponential factor, \( E_a \) is the activation energy, \( k \) is Boltzmann’s constant, and \( T \) is temperature. Advances in material science, such as sulfide-based or oxide-based electrolytes, are driving \( \sigma \) closer to liquid levels, enabling practical solid-state battery designs.

Globally, the solid-state battery ecosystem is shaped by three main player types: dedicated solid-state battery manufacturers, established lithium-ion battery producers, and automotive original equipment manufacturers (OEMs). Each group brings unique strengths to the table, from specialized R&D to mass production expertise and direct integration into vehicles. The following table outlines their roles and typical approaches.

| Player Type | Key Characteristics | Focus Areas |

|---|---|---|

| Dedicated Solid-State Battery Manufacturers | Innovation-driven, agile, often startups | Developing proprietary solid electrolytes, pilot lines |

| Leading Lithium-Ion Battery Manufacturers | Scale advantage, existing supply chains | Integrating solid-state tech into current lines, cost reduction |

| Automotive OEMs | Demand pull, vertical integration | Joint ventures, in-house R&D for vehicle applications |

From a regional perspective, while East Asian nations have dominated traditional lithium-ion battery markets, European and North American entities are aggressively investing in solid-state battery technologies to capture early-mover advantages. This geopolitical dimension adds complexity to the supply chain, with collaborations and competitions unfolding across borders. The solid-state battery, as a key enabler for electric mobility and grid storage, is at the heart of these strategic maneuvers.

Capacity planning for solid-state batteries has surged, with global announcements exceeding 540 GWh. However, given the nascent stage of the market, actual deployment remains uncertain. To quantify this, I estimate the projected capacity growth using a logistic function: $$ C(t) = \frac{C_{\text{max}}}{1 + e^{-k(t-t_0)}} $$ where \( C(t) \) is the capacity at time \( t \), \( C_{\text{max}} \) is the maximum potential capacity, \( k \) is the growth rate, and \( t_0 \) is the inflection point. Based on current trends, \( t_0 \) aligns around 2026, marking the start of the mass production era for solid-state batteries. The table below summarizes aggregated capacity projections by region, avoiding specific company names to adhere to analysis guidelines.

| Region | Planned Capacity (GWh) | Primary Focus |

|---|---|---|

| East Asia | ~300 GWh | Semi-solid and all-solid battery development |

| North America | ~150 GWh | Innovation in solid electrolyte materials |

| Europe | ~90 GWh | Automotive integration and sustainability |

The timeline for mass production of solid-state batteries is a critical metric. Based on public announcements, the period from 2026 onward is expected to witness a gradual ramp-up. Semi-solid batteries are likely to lead the charge, serving as a bridge to all-solid systems. I have constructed a timeline table to encapsulate these milestones, emphasizing the phased approach across player types.

| Time Frame | Development Phase | Key Activities |

|---|---|---|

| 2024-2025 | Pilot and Validation | Factory trials, initial vehicle integrations, performance testing |

| 2026-2027 | Early Mass Production | Semi-solid battery rollout, capacity scaling, cost optimization |

| 2028-2030 | Commercial Expansion | All-solid battery introduction, broader automotive adoption |

| Post-2030 | Maturity and Innovation | Next-gen solid-state battery variants, new applications |

For instance, numerous Chinese manufacturers have targeted 2026 for initial solid-state battery production, with some focusing on semi-solid variants and others advancing all-solid prototypes. In the United States, several companies are building giga-scale facilities slated for operation by 2026, initially producing semi-solid batteries before transitioning to full solid-state systems. Japanese and South Korean players, while slightly more conservative, aim for commercialization by the end of the decade, leveraging their expertise in precision manufacturing. This staggered timeline reflects the technical hurdles, such as interfacial resistance between electrodes and solid electrolytes, which can be modeled as: $$ R_{\text{total}} = R_{\text{bulk}} + R_{\text{interface}} $$ where \( R_{\text{total}} \) is the total resistance, \( R_{\text{bulk}} \) is the electrolyte bulk resistance, and \( R_{\text{interface}} \) is the interfacial resistance. Reducing \( R_{\text{interface}} \) is pivotal for achieving high power densities in solid-state batteries.

The economic implications of solid-state battery adoption are profound. Cost per kilowatt-hour (kWh) is a primary concern, often expressed as: $$ \text{Cost}_{\text{kWh}} = \frac{\text{Material Cost} + \text{Manufacturing Cost}}{\text{Energy Output}} $$ With solid-state batteries, material costs may be higher initially due to exotic electrolytes, but manufacturing simplifications—such as reduced need for cooling systems—could offset this. As production scales, learning curve effects will drive costs down, potentially reaching parity with liquid lithium-ion batteries by the early 2030s. This cost trajectory is essential for enabling downstream applications beyond electric vehicles, including aerospace, medical devices, and grid storage, where the solid-state battery’s safety and energy density are paramount.

Moreover, the rise of solid-state batteries will reshape the manufacturing equipment market. Traditional coating and assembly lines for liquid electrolytes may require retrofitting or replacement with dry-room processes suited for solid electrolytes. The demand for precision stacking, solid electrolyte layer deposition, and quality control tools will surge, creating opportunities for equipment suppliers. This transition underscores the interconnectedness of technology and infrastructure in the solid-state battery ecosystem.

In conclusion, the solid-state battery is on the cusp of transforming energy storage paradigms. From technological breakthroughs to ambitious capacity plans, the momentum is unmistakable. While challenges in material stability, production scalability, and cost reduction persist, the collective efforts of diverse players are paving the way for a mass production era starting around 2026. As a analyst, I anticipate that the solid-state battery will not only enhance existing applications but also unlock novel use cases, driving a more sustainable and efficient energy future. The journey ahead is complex, but the potential rewards—for safety, performance, and environmental impact—make the solid-state battery a cornerstone of next-generation innovation.