As I delve into the evolving landscape of energy storage, it becomes increasingly clear that the solid-state battery represents a pivotal innovation with the potential to revolutionize electric vehicles and beyond. The global competition to develop and commercialize this technology has intensified, with regions like Japan, South Korea, Europe, and the United States pursuing distinct strategies and technical pathways. In this analysis, I aim to explore the progress, challenges, and future prospects of solid-state battery development across these key players, leveraging tables and formulas to summarize critical insights. The journey toward a solid-state battery future is fraught with scientific hurdles, but the rewards—higher energy density, enhanced safety, and longer lifespan—are driving relentless investment and research worldwide.

The concept of a solid-state battery is not new; it has been a subject of academic and industrial interest for decades. Unlike conventional lithium-ion batteries that use liquid electrolytes, solid-state batteries employ solid electrolytes, which can mitigate risks such as leakage, flammability, and dendrite formation. This fundamental shift promises a leap in performance, with energy density potentially exceeding 500 Wh/kg, compared to the current 250-300 Wh/kg for liquid-based systems. From my perspective, the race for solid-state battery supremacy is not just about technological prowess but also about securing economic and strategic advantages in the burgeoning electric mobility sector.

In assessing the global landscape, patent activity serves as a valuable indicator of innovation momentum. Historically, Japanese entities have dominated the intellectual property sphere for solid-state battery technologies, with one major automaker amassing over a thousand patents since the early 2000s, covering aspects from materials to manufacturing processes. This early lead has positioned Japan as a frontrunner, but as I observe, competitors from South Korea, China, Europe, and the U.S. are accelerating their efforts, potentially reshaping the hierarchy. The sheer volume of patents underscores the importance of solid-state battery research, yet practical commercialization remains the ultimate benchmark for success.

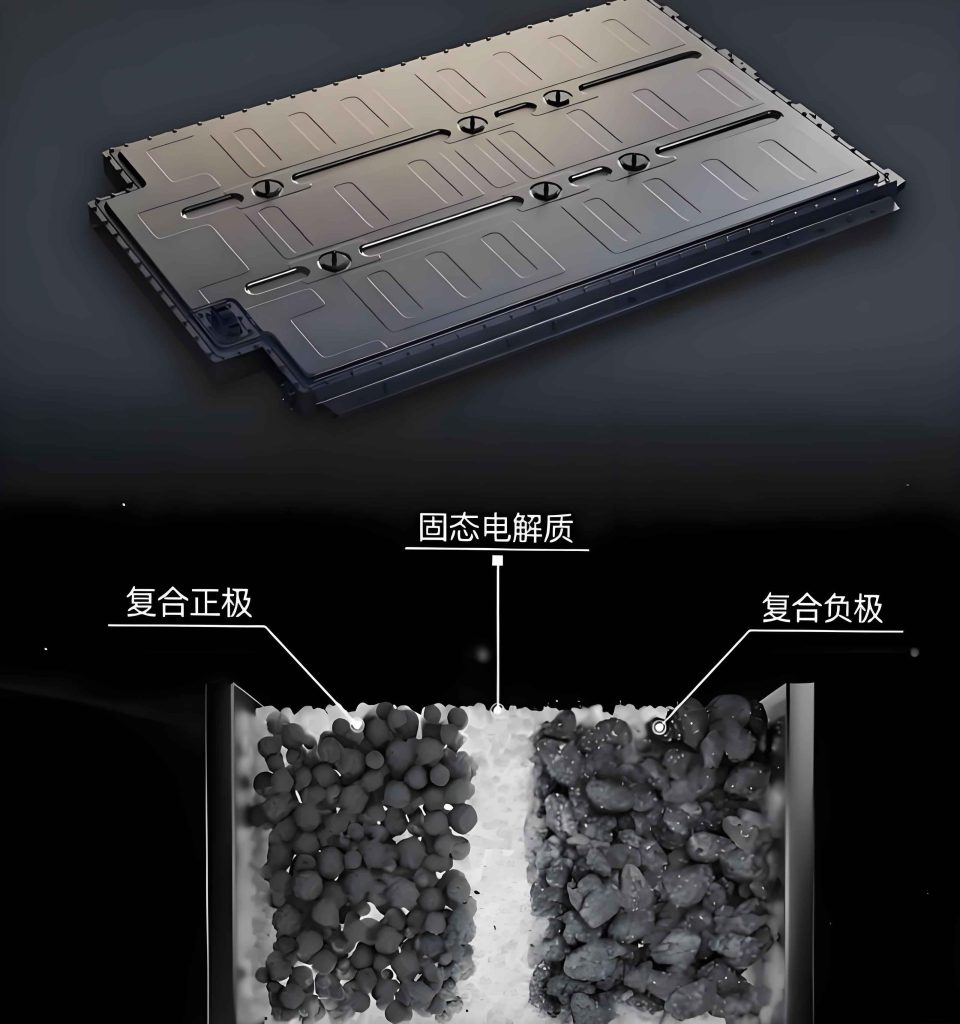

When examining technical routes, solid-state batteries are primarily categorized by electrolyte type: polymer, oxide, and sulfide. Each pathway offers unique trade-offs in terms of ionic conductivity, stability, and manufacturability. Japanese and South Korean firms heavily favor sulfide-based solid-state batteries due to their high ionic conductivity, which can approach that of liquid electrolytes, making them ideal for electric vehicle applications. The ionic conductivity $\sigma$ for sulfide electrolytes can be modeled using the Arrhenius equation: $$\sigma = \sigma_0 \exp\left(-\frac{E_a}{kT}\right)$$ where $\sigma_0$ is the pre-exponential factor, $E_a$ is the activation energy, $k$ is Boltzmann’s constant, and $T$ is temperature. This high conductivity, often exceeding $10^{-2}$ S/cm at room temperature, is a key advantage, but challenges like interfacial instability and moisture sensitivity persist. In contrast, European players tend to focus on polymer-based solid-state batteries, which are easier to process and scale, albeit with lower conductivity limits. American startups often explore oxide or hybrid approaches, seeking a balance between performance and practicality. The table below summarizes the dominant technical routes and their characteristics:

| Electrolyte Type | Advantages | Disadvantages | Key Regions/Players |

|---|---|---|---|

| Sulfide | High ionic conductivity, good mechanical properties | Poor stability in air, expensive raw materials | Japan, South Korea |

| Oxide | Excellent stability, wide electrochemical window | Lower conductivity, brittle nature | U.S., Europe |

| Polymer | Flexible, easy to manufacture, low cost | Low conductivity at room temperature | Europe, some U.S. firms |

Turning to regional progress, Japan’s approach to solid-state battery development is characterized by strong government-industry collaboration and long-term vision. Initiatives like the New Energy and Industrial Technology Development Organization (NEDO) have funneled substantial funding into research consortia involving automakers and material suppliers. A leading Japanese automaker, for instance, aims to deploy sulfide-based solid-state batteries in vehicles by 2030, while a major electronics firm plans to start mass production by the end of this decade. South Korea mirrors this intensity, with its government pledging significant investments to support battery giants in achieving commercialization by 2030. The synergy between Korean battery manufacturers and global automakers is a testament to the strategic importance of solid-state battery technology in securing market leadership.

In Europe, the landscape is more fragmented, with automakers often partnering with American startups to hedge their bets. A German automotive giant, for example, has invested heavily in a U.S.-based solid-state battery developer, conducting endurance tests that demonstrate remarkable longevity—over 500,000 kilometers with minimal capacity fade. This highlights the potential of solid-state battery systems, but European firms remain cautious, citing rapid improvements in conventional lithium-ion batteries that may narrow the performance gap. From my analysis, this pragmatism reflects a wait-and-see attitude, where maintaining a technological foothold is prioritized over aggressive commercialization timelines.

The United States, meanwhile, is a hub of innovation driven by venture-backed startups. Companies are exploring diverse electrolyte chemistries, with some focusing on oxide-based solid-state batteries that offer enhanced safety. A notable startup has delivered prototype cells to European automakers, progressing through testing phases toward potential mass production by 2026. The energy density of these solid-state battery prototypes can be estimated using the formula: $$E_d = \frac{C \times V}{m}$$ where $E_d$ is the gravimetric energy density (Wh/kg), $C$ is the capacity (Ah), $V$ is the average voltage (V), and $m$ is the mass (kg). For instance, if a solid-state battery cell has a capacity of 100 Ah, a voltage of 3.6 V, and a mass of 0.5 kg, the energy density calculates to: $$E_d = \frac{100 \times 3.6}{0.5} = 720 \text{ Wh/kg}$$ Such values, though theoretical, underscore the transformative potential of solid-state battery technology.

To provide a comprehensive overview, I have compiled a table detailing the产业化进展 of key enterprises across Japan, South Korea, Europe, and the United States. This table encapsulates their chosen solid-state battery routes, current研发进展, and projected timelines, drawing from public announcements and industry reports. It is evident that the solid-state battery race is a marathon, not a sprint, with milestones spread over the coming decade.

| Country/Region | Company | Solid-State Battery Technology Route | Research and Development Progress |

|---|---|---|---|

| Japan | A leading automaker | Sulfide | Planning to install sulfide solid-state batteries in vehicles by 2030; extensive patent portfolio and material advancements. |

| Japan | A major electronics corporation | Sulfide | Publicly demonstrated prototypes in 2023; targeting mass production by 2029. |

| Japan | An automotive alliance member | Sulfide | Piloting production in 2025, with full-scale electric vehicle launch expected around 2028. |

| Japan | A chemical company | Sulfide | Initiating large-scale electrolyte production verification in 2024 to support supply chains. |

| South Korea | A battery manufacturer | Sulfide, Polymer | Completed pilot line in 2023; developing large-cell technology for 2025, with mass production by 2027. |

| South Korea | Another battery giant | Sulfide, Polymer | Established semi-solid battery production in 2023; aiming for commercial polymer-based variants by 2026. |

| South Korea | A third battery player | Sulfide | Targeting early prototypes by 2026 and commercialization by 2028. |

| Europe | An automotive alliance partner | Polymer | Planning cobalt-free solid-state battery integration by 2025, leveraging external tech support. |

| Europe | An industrial group | Polymer | Achieved small-scale production of low-energy-density solid-state batteries in 2011; ongoing R&D for automotive grades. |

| United States | A startup | Sulfide | Delivered first samples to a European automaker in 2023; validation phase ongoing, with mass production eyed for 2026. |

| United States | Another startup | Not specified | Supplied advanced prototype cells to a European luxury automaker in 2024 for extensive testing. |

| United States | A third startup | Oxide | Aiming to establish a production line by 2025, backed by major automotive investments. |

Delving deeper into the scientific challenges, the interface between solid electrolytes and electrodes is a critical bottleneck for solid-state battery performance. The interfacial resistance $R_i$ can be described by: $$R_i = \frac{\delta}{\sigma_i A}$$ where $\delta$ is the interfacial layer thickness, $\sigma_i$ is the interfacial conductivity, and $A$ is the contact area. Minimizing $R_i$ is essential for achieving high power density in solid-state battery systems. Moreover, the volumetric energy density $\rho_E$ is a key metric, given by: $$\rho_E = \frac{E}{V} = \frac{\int V \, dQ}{V}$$ where $E$ is energy, $V$ is volume, and $Q$ is charge. Solid-state batteries promise significant improvements here, potentially doubling or tripling values compared to incumbent technologies.

In Japan and South Korea, the focus on sulfide electrolytes stems from their ability to address interfacial issues through material engineering. For example, doping strategies can enhance ionic conductivity, as shown in the formula for conductivity enhancement: $$\sigma_{\text{enhanced}} = \sigma_{\text{base}} + \alpha x$$ where $\alpha$ is a doping coefficient and $x$ is the dopant concentration. Government-led projects in these regions aim to accelerate such innovations, with national strategies outlining ambitious targets for domestic production capacity—envisioning hundreds of gigawatt-hours annually by 2030. This coordinated effort underscores the systemic approach to solid-state battery development, where supply chain resilience and technological sovereignty are paramount.

Conversely, in Europe and the U.S., the emphasis is often on incremental innovation and partnerships. European automakers, while optimistic about solid-state battery potential, acknowledge that conventional lithium-ion advancements may delay widespread adoption. A senior executive from a German luxury carmaker recently noted that energy density gains in liquid batteries have been surprisingly robust, potentially reducing the urgency for solid-state battery deployment. However, this hasn’t halted investments; instead, it has fostered a diversified portfolio where solid-state battery research proceeds in parallel with other technologies. This pragmatic stance is reflected in the steady flow of prototype deliveries and testing milestones, ensuring that these regions remain contenders in the solid-state battery arena.

The economic implications of solid-state battery commercialization are profound. Cost reduction is a major hurdle, as solid-state battery production currently involves expensive materials and complex processes. The total cost $C_{\text{total}}$ can be modeled as: $$C_{\text{total}} = C_{\text{materials}} + C_{\text{manufacturing}} + C_{\text{R&D}}$$ where material costs dominate, especially for sulfide electrolytes requiring rare elements. Scaling production to achieve economies of scale is crucial, with learning curve effects potentially driving down costs over time. Industry analysts project that solid-state battery prices could fall below $100/kWh by 2030 if breakthroughs in material synthesis and cell design materialize.

Looking ahead, the timeline for widespread solid-state battery adoption remains uncertain. Most experts agree that the 2020s will be a decade of refinement and pilot projects, with mass market penetration likely in the 2030s. Key milestones to watch include the transition from laboratory-scale cells to automotive-grade modules, the establishment of robust supply chains for solid electrolytes, and the resolution of durability issues in real-world conditions. As I synthesize these insights, it is clear that the solid-state battery revolution will be a gradual process, shaped by regional strategies, technological breakthroughs, and market dynamics.

In conclusion, the global race for solid-state battery technology is a multifaceted endeavor, with Japan and South Korea pursuing aggressive, government-backed roadmaps centered on sulfide electrolytes, while Europe and the United States adopt more cautious, partnership-driven approaches. The repeated emphasis on solid-state battery innovation across regions highlights its transformative potential, but challenges in materials science, manufacturing, and cost must be overcome. Through tables and formulas, I have summarized the progress and technical nuances, illustrating that while the path to commercialization is complex, the pursuit of solid-state battery supremacy will undoubtedly reshape the future of energy storage. As developments unfold, continuous monitoring of these dynamics will be essential for stakeholders across the industry.