As a researcher focused on energy transition and industrial policy, I have been closely monitoring the rapid evolution of the solid-state battery sector. Solid-state batteries are widely regarded as one of the ultimate technologies to address the range anxiety of new energy vehicles (NEVs), and the recent deployment of the world’s first mass-production line has significantly accelerated their commercialization. In this analysis, I will explore the current state, challenges, and future prospects of the solid-state battery industry in Beijing, leveraging data, tables, and formulas to provide a comprehensive overview. The term ‘solid-state battery’ will be emphasized throughout to underscore its critical role.

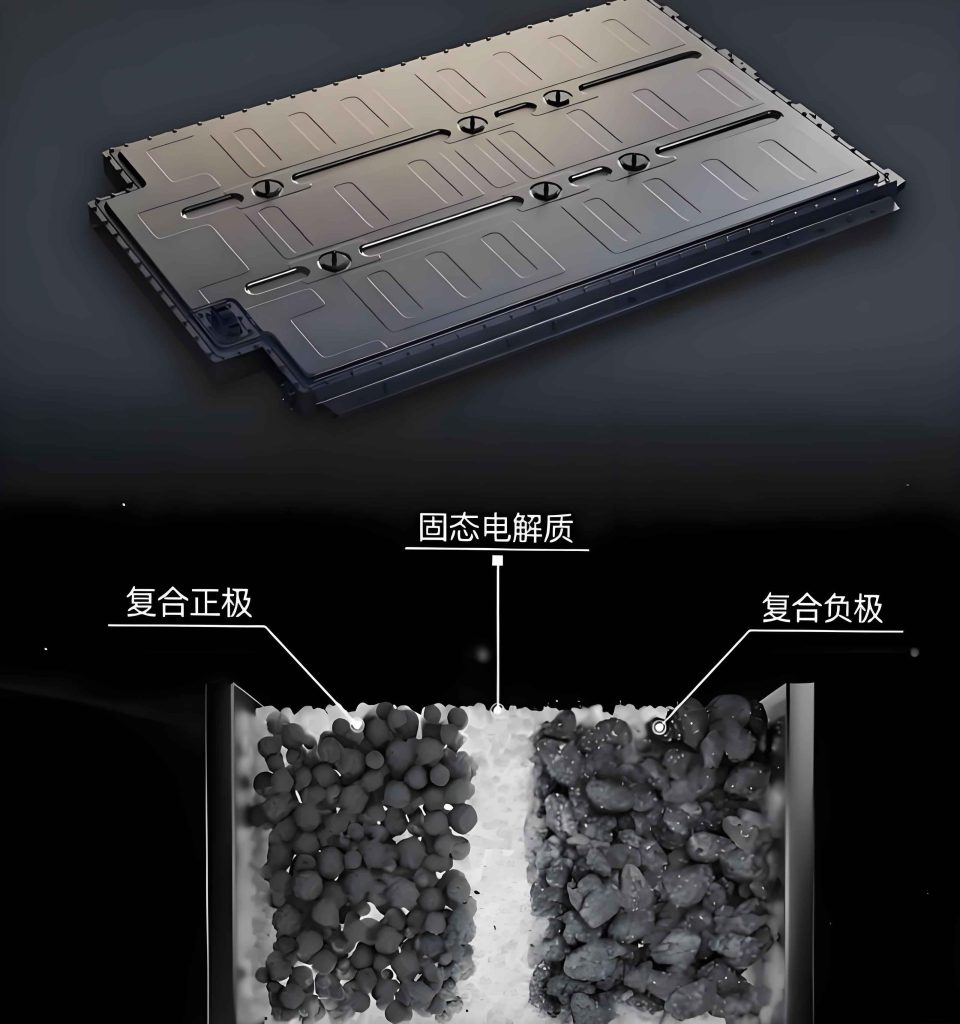

The advent of solid-state batteries marks a paradigm shift in energy storage technology. Compared to traditional liquid lithium-ion batteries, solid-state batteries offer transformative improvements in safety, energy density, and operational robustness. These advantages stem from the replacement of flammable liquid electrolytes with solid electrolytes, which inherently reduce risks of leakage, thermal runaway, and oxidation. The fundamental performance comparison can be summarized in the table below:

| Attribute | Liquid Lithium-ion Battery | Solid-State Battery |

|---|---|---|

| Electrolyte | Organic solvent + LiPF6 + additives | Polymer, oxide, or sulfide solid electrolyte |

| Separator | Liquid separator | None required |

| Thermal Stability | Up to 100°C | Up to 800°C |

| Energy Density | < 300 Wh/kg | > 500 Wh/kg |

| Operating Temperature | -10°C to 45°C | -30°C to 100°C |

| Cycle Life (Charges) | ~2000 cycles | ~10000 cycles |

| Safety | Lower due to flammable solvents | Higher due to non-flammable solid electrolytes |

The energy density advantage is particularly crucial for NEVs, as it directly impacts driving range. A simple formula to estimate the range extension potential is:

$$ \Delta R = \frac{E_{\text{solid}} – E_{\text{liquid}}}{E_{\text{liquid}}} \times R_{\text{base}} $$

where \( \Delta R \) is the increase in range, \( E_{\text{solid}} \) and \( E_{\text{liquid}} \) are the energy densities of solid-state and liquid batteries respectively, and \( R_{\text{base}} \) is the base range with liquid batteries. Given \( E_{\text{solid}} \approx 500 \, \text{Wh/kg} \) and \( E_{\text{liquid}} \approx 250 \, \text{Wh/kg} \), the range can potentially double, making solid-state batteries a game-changer.

Globally, research and development in solid-state batteries are concentrated in several key regions, each pursuing distinct technical pathways. The primary solid-state battery technologies can be categorized into three routes: polymer, oxide, and sulfide. Each has unique strengths and weaknesses, as outlined below:

| Country/Region | Primary Technology Route | Advantages | Disadvantages | Representative Entities |

|---|---|---|---|---|

| Europe & USA | Polymer-based all-solid-state battery | Easy processing, compatibility with existing production equipment, good mechanical flexibility | Lower thermal stability (~200°C), lower energy density, prone to electrolysis at high voltage differentials | Solid Power (USA) |

| China (current focus) | Oxide-based semi-solid-state battery | High thermal stability (up to 1000°C), strong conductivity, good mechanical properties, scalable preparation | High porosity may hinder ion transport, often requires liquid electrolytes for semi-solid versions | Weilan New Energy, Qingtao Energy |

| Japan & South Korea | Sulfide-based all-solid-state battery | Strong thermal stability (400-600°C), electrolytes resistant to electrolysis | Complex manufacturing processes, high production costs | Toyota, Samsung SDI |

From my perspective, the global产业化进程 for solid-state batteries is accelerating, with key milestones shaping the competitive landscape. The first mass-production line for all-solid-state batteries, launched in late 2023, has heightened expectations for commercialization. However, the timeline varies across regions. A projected roadmap for all-solid-state battery development among leading global players is illustrated below:

| Country | Key Enterprises | Current产业化 Progress | Future Targets |

|---|---|---|---|

| Japan | Toyota, Nissan | Overcome technical bottlenecks, prototype batteries with 10-minute charge for 1200 km range | Mass production by 2027-2030 |

| South Korea | Samsung SDI, SK On, LG Energy Solution | Substantial progress in all-solid-state R&D, pilot lines established | Commercialization by 2030 |

| USA | Quantum Scape, Solid Power | Entered A-sample validation stage, collaboration with European automakers | Mass production by 2026-2028 | China | Weilan New Energy, Qingtao Energy, CATL | Semi-solid-state batteries in mass production; all-solid-state in lab stage | Aim for all-solid-state量产 by 2030 |

The progress can be modeled using a technology readiness level (TRL) scale, where TRL 1 represents basic research and TRL 9 signifies full commercialization. For solid-state batteries, the global average TRL is around 5-6, indicating prototype development and pilot testing. The evolution rate \( \frac{d(\text{TRL})}{dt} \) is influenced by R&D investment \( I \) and policy support \( P \), expressed as:

$$ \frac{d(\text{TRL})}{dt} = k \cdot I^\alpha \cdot P^\beta $$

where \( k \), \( \alpha \), and \( \beta \) are constants reflecting innovation efficiency. This highlights the importance of sustained investment and supportive policies for advancing solid-state battery technology.

Turning to Beijing, I observe that the city possesses a robust foundation for solid-state battery development. The industrial chain is relatively complete, spanning from raw materials and R&D to manufacturing and applications. Key players include Weilan New Energy, a leading enterprise that has achieved mass production of semi-solid-state batteries with energy densities exceeding 360 Wh/kg. Additionally, Beijing hosts prestigious research institutions such as Beijing Institute of Technology, Chinese Academy of Sciences, and Beijing University of Science and Technology, which contribute cutting-edge research in solid-state electrochemistry. The city’s focus on新能源车产业发展 aligns well with the high safety and performance of solid-state batteries, offering a strong支撑 for future growth.

However, through my analysis, several challenges must be addressed to solidify Beijing’s position in the solid-state battery arena. First, the R&D门槛 for all-solid-state batteries remains high, and the commercialization cycle is relatively long, often exceeding 5-8 years. Current policy support in Beijing is limited compared to international counterparts. For instance, Japan has allocated over ¥200 billion (approx. $1.4 billion) through government-industry-academia alliances, while South Korea offers tax incentives, and Germany funds projects with millions of euros. In contrast, China has yet to introduce专项补贴 policies for solid-state batteries, and Beijing lacks targeted initiatives, potentially slowing progress.

Second, the布局力度 in frontier research is insufficient. Although Beijing has strong academic resources, its patent output in solid-state batteries lags behind global leaders. Japan holds about 68% of global all-solid-state battery patents, with Toyota alone owning nearly 1400 patents. The USA and South Korea follow with 16% and 12% respectively. In China, the top patent-holder has around 100 patents, while Beijing-based Weilan New Energy仅 has 6 authorized patents. Other local firms like BTR New Material and Ronbay Technology primarily focus on liquid lithium batteries, missing opportunities in the solid-state domain. This gap can be quantified using a patent concentration index \( C \):

$$ C = \frac{\sum_{i=1}^n s_i^2}{N} $$

where \( s_i \) is the share of patents held by entity \( i \), and \( N \) is the total number of entities. For solid-state batteries, Japan’s high \( C \) indicates dominance, whereas Beijing’s low \( C \) suggests fragmented innovation.

Third, the领军企业 in Beijing have not fully manifested their带动作用 on the产业链 and industrial agglomeration. While Weilan New Energy ranks among China’s top five solid-state battery firms with a valuation around ¥15.7 billion and projected revenue growth to ¥10 billion by 2025, its impact on upstream and downstream segments is limited. Data shows that Beijing has only 47 solid-state battery-related enterprises, fewer than Jiangsu (68) and Guangdong (85). Among 87 listed companies in China’s solid-state battery sector, Beijing仅有 has 5, compared to 25 in Guangdong and 12 in Zhejiang. Moreover, Beijing has only one major固态电池 base (Zhongguancun Fangshan Park), versus ten liquid lithium battery bases. This disparity hinders集群效应 formation, which is essential for reducing costs via economies of scale. The cost reduction potential can be expressed as:

$$ C_{\text{unit}} = C_0 \cdot Q^{-\eta} $$

where \( C_{\text{unit}} \) is the unit cost, \( C_0 \) is the initial cost, \( Q \) is the cumulative production, and \( \eta \) is the learning rate (typically 0.1-0.3 for batteries). Without strong industrial clusters, \( Q \) grows slowly, keeping \( C_{\text{unit}} \) high for solid-state batteries.

Based on these insights, I propose several policy recommendations to foster the solid-state battery industry in Beijing. First,全力支持 technological突破 is crucial. The city should integrate solid-state battery攻关 into its top-level designs, such as the “15th Five-Year Plan” for International Science and Technology Innovation Center construction. Dedicated funds should support key technology攻克, production equipment, and process optimization. Additionally, promoting产学研协同创新 through platforms like the “China All-Solid-State Battery Industry-University-Research Collaborative Innovation Platform (CASIP)” can enhance knowledge sharing and joint R&D in areas like electrode materials, cell design, and manufacturing techniques.

Second,务实支持 production环节落地 in Beijing is essential. Encouraging partnerships between local automakers (e.g., BAIC BluePark, Li Auto, Xiaomi) and solid-state battery firms like Weilan New Energy and CATL can expedite产业化项目. Existing projects, such as Weilan’s solid-state lithium-ion battery产业化 project in Fangshan and CATL’s cell factory Phase I, should be accelerated, with consideration for additional production lines in平原新城 like Shunyi and Changping. To strengthen the ecosystem,培育壮大中腰部企业及上下游配套企业 is vital. Leveraging demonstration effects from bases like Weilan’s production facility and BTR’s engineering centers can attract更多专精特新 and gazelle firms. Furthermore, supporting京津冀协同 to cultivate industrial clusters through joint investment promotion and project sharing can amplify规模效应.

Third,多方位聚能服务涵养产业生态 will ensure sustainable growth. This includes加大高层次人才引进力度, offering housing and education benefits to attract experts in solid-state battery fields. Optimizing the投融资环境 by including eligible solid-state battery enterprises in the北京交易所上市企业储备库 for listing services, and encouraging金融机构 to provide equity-loan联动 and other financial products, can alleviate capital constraints. Utilizing platforms like “北京畅融工程” for银企对接 can improve access to融资政策. Lastly, incorporating key solid-state battery firms into “服务包” programs with tailored诉求清单 and problem-solving mechanisms can provide管家式服务, enhancing operational efficiency.

In conclusion, the development of the solid-state battery industry in Beijing holds significant promise for advancing the city’s新能源车产业 and energy transition goals. By addressing R&D gaps, strengthening production capabilities, and fostering a supportive ecosystem, Beijing can position itself as a leader in this transformative technology. The journey requires concerted efforts from government, industry, and academia, with continuous emphasis on innovation and collaboration. As solid-state batteries evolve, their impact on safety, performance, and sustainability will redefine the future of energy storage, making them a cornerstone of Beijing’s industrial strategy.