As global emphasis on environmental protection and sustainable development intensifies, the energy system is rapidly transitioning toward clean, green, and low-carbon solutions. New energy vehicles, as a green mode of transportation, are becoming mainstream in future mobility. Among the core technologies for these vehicles, battery systems are critical. Currently, traditional liquid lithium-ion batteries have an energy density ceiling of approximately 300 Wh/kg, which struggles to meet the demand for long driving ranges in new energy vehicles. Additionally, the flammable and volatile nature of liquid electrolytes poses significant safety risks, such as thermal runaway under extreme conditions like high temperatures, short circuits, or overcharging.

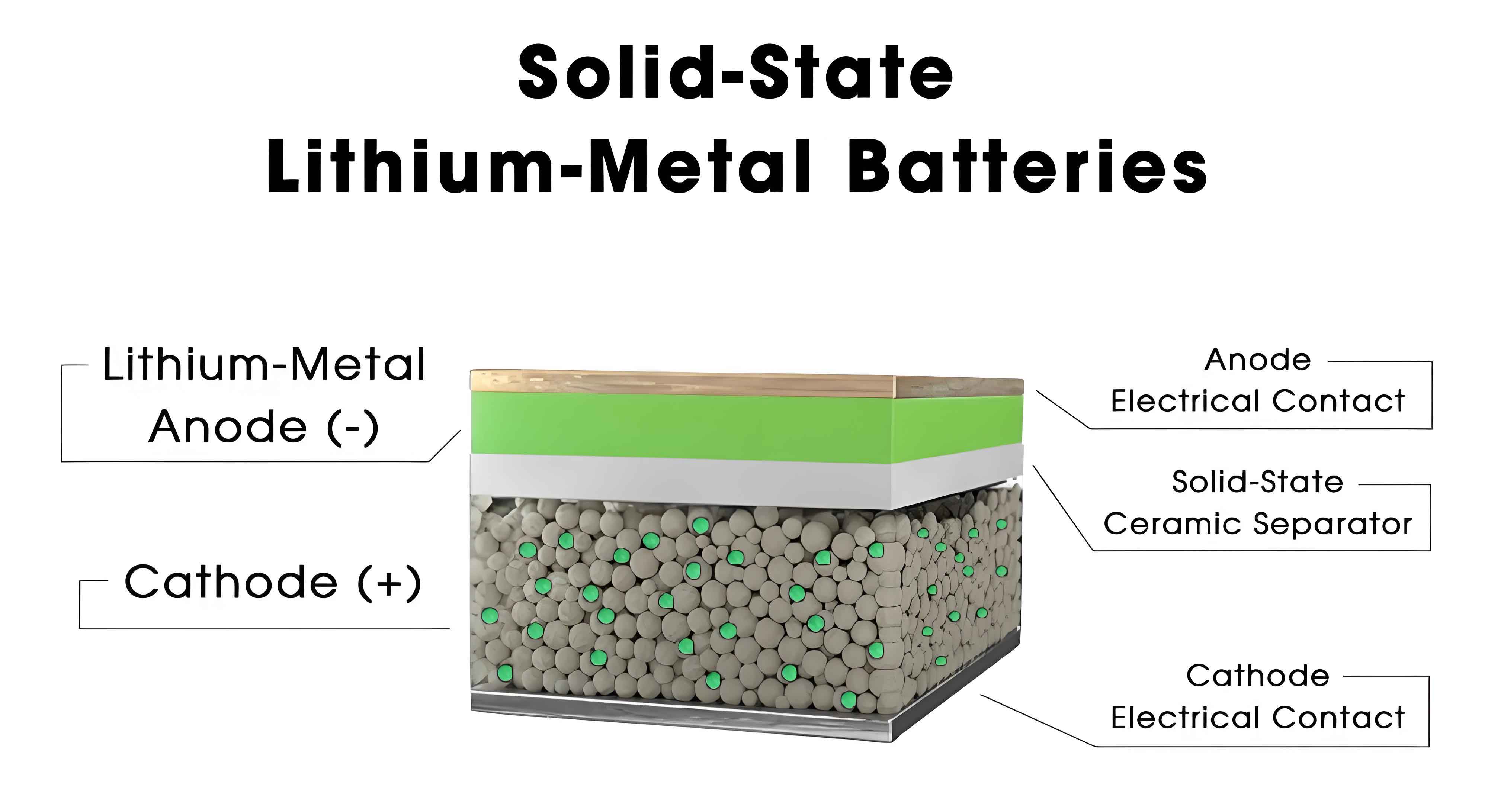

Solid state batteries, as a novel battery form contrasting with liquid batteries, replace traditional liquid electrolytes with solid-state electrolytes. This fundamentally addresses safety issues like combustion or explosions caused by organic electrolyte leakage in conventional batteries. With significant advantages in energy density, safety, and cycle stability, solid state batteries are regarded as the ideal choice for next-generation power batteries. They hold strategic importance for enhancing overall battery technology and advancing fields like electric transportation and energy storage systems.

In this context, solid-state electrolytes are the core components of solid state batteries. To promote high-quality development in the solid state battery industry, we conducted an in-depth analysis of domestic and international invention and utility model patents related to solid-state electrolytes. This study systematically examines global and Chinese patent application trends, differences in technological layouts among China, the U.S., Japan, and South Korea, dynamics of key global applicants, research progress across various technical branches, and critical patents from major applicants. Through this patent-based perspective, we aim to provide decision-making support for technological research and development in related enterprises, thereby enhancing innovation efficiency across the industry.

Patent Research Objects and Methods

To better delineate the specifics of each technical branch in the solid-state electrolyte industry chain, we performed a patent technology decomposition for solid-state electrolytes. By combining literature reviews and interviews with industry experts, we systematically classified solid-state electrolyte materials and developed a corresponding technology decomposition table, as detailed below.

| Primary Branch | Secondary Branch |

|---|---|

| Polymer Solid-State Electrolytes | Polyethylene Oxide-Based Solid-State Electrolytes |

| Other Polymer-Based Solid-State Electrolytes | |

| Organic-Inorganic Composite Solid-State Electrolytes | |

| Oxide Solid-State Electrolytes | Perovskite Type: e.g., Lithium Lanthanum Titanate (LLTO) |

| Sodium Superionic Conductor Type: e.g., Lithium Aluminum Titanium Phosphate/Lithium Aluminum Germanium Phosphate (LATP/LAGP) | |

| Lithium Superionic Conductor Type: e.g., Lithium Zirconium Gallium Oxide (LZGO) | |

| Garnet Type: e.g., Lithium Lanthanum Zirconium Oxide (LLZO) | |

| Sulfide Solid-State Electrolytes | Crystalline: e.g., Lithium Germanium Phosphorus Sulfide (LGPS Type), Argyrodite Type LiPSX (X is Halogen) |

| Glass State: e.g., Li2S-MxSy (M is Aluminum, Silicon, Phosphorus, Tin) | |

| Glass-Ceramic State: e.g., Li7P3S11 |

Based on Table 1, solid-state electrolytes are primarily categorized into three technical branches: polymer, oxide, and sulfide solid-state electrolytes. Each type has distinct advantages and disadvantages. Polymer solid-state electrolytes offer good flexibility, ease of processing, and low interfacial resistance, but they typically exhibit low ionic conductivity at room temperature and are prone to oxidation under high voltage, making them unsuitable for use with high-voltage cathode materials. The ionic conductivity of polymer electrolytes can be modeled using the Arrhenius equation: $$ \sigma = A \exp\left(-\frac{E_a}{kT}\right) $$ where $\sigma$ is the ionic conductivity, $A$ is the pre-exponential factor, $E_a$ is the activation energy, $k$ is Boltzmann’s constant, and $T$ is the temperature. Oxide solid-state electrolytes boast excellent air stability, high chemical and electrochemical stability, and non-flammability. Their high mechanical strength effectively inhibits lithium dendrite growth. However, their rigidity and brittleness make large-scale production of ultra-thin solid-state electrolytes challenging. Moreover, they suffer from low ionic conductivity and high interfacial resistance. Sulfide solid-state electrolytes have ionic conductivity nearly comparable to traditional liquid electrolytes and excellent flexibility, allowing easy integration into all-solid-state lithium batteries via simple cold pressing. Nevertheless, they exhibit poor air stability, reacting with water to produce toxic gases like H2S, and have low oxidation potential, leading to interfacial reactions with cathode materials.

For our research, patent data was sourced from the Heima Global Patent Search and Analysis Platform. Based on the technical characteristics of solid state batteries and the results of the solid-state electrolyte technology decomposition, we extracted relevant keywords and constructed patent search expressions using International Patent Classification codes. The search was conducted up to December 30, 2024. Given that invention patent applications typically require 18 months from the filing date (or priority date) to be published, and utility model patents are published only after authorization, data from 2023-2024 lacks full statistical significance and is included for reference only. We retrieved patent data from the past 20 years, applying noise reduction to eliminate duplicates and irrelevant patents, ensuring the accuracy of subsequent analysis.

Patent Competition Landscape Analysis

Analysis of Patent Application Trends

The trends in global and Chinese patent applications for solid-state electrolytes reveal distinct phases of development. The solid state battery industry has evolved through several clear stages, as illustrated in the data below.

| Period | Global Applications | Chinese Applications | Characteristics |

|---|---|---|---|

| 2005-2010 | Slow growth, ~10% annual increase | Similar slow growth | Technology accumulation phase; early R&D with limited patents |

| 2011-2015 | Accelerated growth, peak of 2,197 in 2015 | Rise to 380 in 2015 | Slow development phase; gradual maturation and increased focus |

| 2016-Present | Rapid growth, peak of 6,542 in 2022 | Peak of 2,369 in 2022, 2,436 in 2023 | High-speed development phase; explosive growth driven by technological breakthroughs |

In the technology accumulation period (2005-2010), global and Chinese patent numbers grew gradually, with an average annual increase of about 10%. Solid-state electrolyte technology was in its early R&D stage, with few patents concentrated in basic research areas. Technical challenges, such as conductivity and stability in all-solid-state batteries, resulted in slow growth. During the slow development period (2011-2015), patent numbers accelerated globally and in China, reaching 2,197 global and 380 Chinese applications by 2015. Breakthroughs in electrolyte materials and battery design fueled this growth. In the high-speed development period (2016-present), patent numbers exploded, with global applications surging to 6,542 in 2022 and Chinese applications to 2,369 in 2022 and 2,436 in 2023. This phase was driven by the approaching theoretical energy density limit of liquid batteries, necessitating higher-density alternatives, alongside core technology advancements in solid-state electrolytes, anodes, and cathodes. As technical hurdles were overcome, innovation shifted toward optimization and industry chain integration, further boosting patent activity. The growth in solid state battery patents underscores the industry’s rapid evolution and the critical role of solid-state electrolytes in enabling next-generation energy storage solutions.

Analysis of Applications by Source Countries

Patent applications for solid state batteries are predominantly concentrated in China, the United States, Japan, and South Korea. The trends over the past 20 years reveal significant shifts in technological development among these key regions.

| Year Range | Japan | United States | South Korea | China | European Patent Office |

|---|---|---|---|---|---|

| 2005-2010 | Leading, slow growth | Second, slow growth | Minor applications | Minor applications | Stable low numbers |

| 2011-2015 | Continued leadership | Steady increase | Rapid growth | Accelerated growth | Moderate growth |

| 2016-2024 | High activity, surpassed by China in 2023 | Consistent applications | Strong growth | Explosive growth, leader by 2023 | Gradual increase |

From 2005 to 2010, Japan and the U.S. led in solid-state electrolyte patents, with Japan in first place and the U.S. second, while applications from other regions were minimal. This period represented a slow development phase with limited global engagement. After 2010, increased innovation incentives, particularly in South Korea and China, spurred rapid growth. By 2015, China’s patent numbers rose significantly, overtaking South Korea in 2016 to become third globally, followed by explosive growth with annual rates of 20-30%. In 2022, China’s applications nearly matched Japan’s, and by 2023, China surpassed Japan to lead globally. This surge from 2015 to 2024 highlights China’s emergence as the hottest market for solid-state electrolytes, driven by policy support and market forces. As China’s technological innovation capabilities advance, it demonstrates increasing competitive advantages in new industries like solid state batteries. The competition in solid state battery technologies is intensifying, with China and Japan leading in different aspects, shaping the future of this critical field.

Analysis of Global Key Applicants

The top global applicants in the solid-state electrolyte field reflect the dominance of Japanese and Korean entities, with no Chinese innovators in the top ten. This indicates the technological leadership of these regions and the need for Chinese firms to enhance their global patent strategies.

| Rank | Applicant | Total Patent Applications | Country |

|---|---|---|---|

| 1 | Toyota Motor Corporation | 4,113 | Japan |

| 2 | Panasonic Group (including Panasonic IP Management and Panasonic Electric Industries) | 3,067 | Japan |

| 3 | LG Group (including LG Chem and LG Energy Solution) | 2,332 | South Korea |

| 4 | Samsung Group (including Samsung SDI and Samsung Electronics) | 1,103 | South Korea |

| 5 | NGK Insulators, Ltd. | 1,013 | Japan |

As shown in Table 4, Toyota Motor Corporation leads with 4,113 applications, followed by the Panasonic Group with 3,067, the LG Group with 2,332, the Samsung Group with 1,103, and NGK Insulators with 1,013. This concentration underscores the advantage of Japanese and Korean companies in solid-state electrolyte technology. Although Chinese applicants have seen explosive growth in patent filings from 2015 to 2024, they started later and lack large-scale, globally leading enterprises. Basic patents in this field are held by foreign entities, posing potential intellectual property risks for Chinese firms expanding overseas. The solid state battery industry requires long-term investment, and Chinese companies must accelerate innovation to catch up, leveraging domestic supply chains and market size. The absence of Chinese applicants in the top global rankings highlights the urgency for strategic patent布局 and R&D enhancements to compete effectively in the global solid state battery market.

Analysis of Key Applicants in China

In China, the patent landscape for solid-state electrolytes includes both international and domestic players, with Japanese and Korean companies actively布局 the market, reflecting confidence in its future potential.

| Rank | Applicant | Patent Applications in China | Country/Region |

|---|---|---|---|

| 1 | Toyota Motor Corporation | 650 | Japan |

| 2 | Panasonic Intellectual Property Management Co., Ltd. | 416 | Japan |

| 3 | Honda Motor Co., Ltd. | 191 | Japan |

| 4 | LG Chem Ltd. | 177 | South Korea |

| 5 | Central South University | 170 | China |

| 6 | Hyundai Motor Company | Data not specified | South Korea |

| 7 | Institute of Physics, Chinese Academy of Sciences | Data not specified | China |

| 8 | Harbin Institute of Technology | Data not specified | China |

| 9 | LG Energy Solution, Ltd. | Data not specified | South Korea |

| 10 | BYD Company Limited | Data not specified | China |

From Table 5, Toyota leads with 650 applications in China, followed by Panasonic with 416, Honda with 191, LG Chem with 177, and Central South University with 170. This shows that Japanese and Korean firms have heavily invested in patent布局 in China, anticipating growth in the solid state battery sector. Meanwhile, Chinese research institutions and companies like Central South University, the Institute of Physics (Chinese Academy of Sciences), Harbin Institute of Technology, and BYD have also established significant presence. Although Chinese innovators lack first-mover advantage, they can leverage opportunities from technological iterations and industry transformations. By learning from Japanese and Korean experiences, Chinese entities can enhance R&D through enterprise-led initiatives and collaborations with research institutes, effectively utilizing talent and resources to drive innovation. The active participation of domestic players in China’s market is crucial for catching up in the solid state battery race, and fostering such partnerships will be key to achieving technological breakthroughs and high-quality development.

Patent Layout Analysis of Solid-State Electrolyte Technical Branches

Application Trend Analysis by Technical Branch

The patent application trends for the three main types of solid-state electrolytes—polymer, oxide, and sulfide—show distinct evolutionary patterns, reflecting their technological maturity and industry focus.

| Year Range | Polymer Electrolyte Applications | Oxide Electrolyte Applications | Sulfide Electrolyte Applications | Key Observations |

|---|---|---|---|---|

| 2005-2007 | Early布局, steady growth | Minor applications | Very low, under 50 | Polymer branch most mature initially |

| 2008-2017 | Gradual increase | Slow growth to under 500 | Slow growth to under 500 | Oxide and sulfide gain traction; key applicants: Toyota, LG |

| 2018-2024 | Peak of 1,961 in 2022 | Peak of 1,572 in 2022 | Peak of 1,821 in 2022 | Explosive growth post-2017; all branches see rapid innovation |

Polymer solid-state electrolytes were the earliest to see patent布局, with a more mature industry chain. From 2005 to 2007, sulfide electrolyte patents were minimal, numbering in the tens. Between 2008 and 2017, oxide and sulfide electrolytes experienced slow growth, with applications staying below 500, primarily from companies like Toyota and LG. After 2017, all three branches saw significant increases, with peaks in 2022: polymer at 1,961, oxide at 1,572, and sulfide at 1,821 applications. This surge aligns with broader advancements in solid state battery technologies, as core issues like conductivity and stability were addressed, shifting innovation toward optimization. The growth trends highlight the dynamic nature of the solid state battery industry, with each electrolyte type contributing to the overall progress. The ionic conductivity for these electrolytes can be expressed using the Nernst-Einstein relation: $$ \sigma = \frac{n q^2 D}{kT} $$ where $\sigma$ is the conductivity, $n$ is the charge carrier density, $q$ is the charge, $D$ is the diffusion coefficient, $k$ is Boltzmann’s constant, and $T$ is the temperature. This formula underscores the importance of material properties in enhancing performance for solid state batteries.

Regional Distribution Analysis by Technical Branch

The geographical distribution of patent applications across the technical branches reveals strategic focuses of different countries, particularly China and Japan, in the development of solid-state electrolytes for solid state batteries.

| Technical Branch | China | Japan | United States | South Korea | European Patent Office |

|---|---|---|---|---|---|

| Polymer Electrolytes | 5,812 | Moderate | Significant | Moderate | Low |

| Oxide Electrolytes | 4,106 | 4,125 | Moderate | Significant | Low |

| Sulfide Electrolytes | Moderate | 5,723 | Low | Significant | Low |

As shown in Table 7, polymer solid-state electrolytes are a foundational focus, with China leading in applications at 5,812, indicating a preference for developing relatively easier-to-commercialize polymer electrolytes. In oxide solid-state electrolytes, Japan and China have comparable布局, with 4,125 and 4,106 applications respectively, reflecting shared optimism about their prospects. For sulfide solid-state electrolytes, Japan dominates with 5,723 applications, far exceeding other regions, underscoring its emphasis on sulfide development. This distribution aligns with national strategies and resource allocations, influencing the global competition in solid state batteries. The varying focuses suggest that while China excels in polymer and competes closely in oxides, Japan’s strength in sulfides could give it an edge in high-performance applications. Understanding these regional disparities is essential for stakeholders aiming to navigate the solid state battery landscape and foster collaborative innovations.

Analysis of Key Applicant Patents

By examining key applicants, their patent families, and citation counts, we can identify critical innovations in solid-state electrolytes. This analysis focuses on Toyota Motor Corporation, LG Group, and the Institute of Physics, Chinese Academy of Sciences, highlighting their contributions to advancing solid state battery technologies.

| Applicant | Patent Number | Application Year | Technical Branch | Citations | Family Countries/Regions | Key Disclosure |

|---|---|---|---|---|---|---|

| Toyota Motor Corporation | CN102696141B | 2010 | Sulfide | 268 | CN, US, EP, JP, KR, WO, DE, AU | Method to produce sulfide solid electrolyte with minimal H2S generation via two-step glassification |

| CN103650231B | 2012 | Sulfide | 193 | CN, US, EP, JP, KR, WO, DE, CA, AU, BR | High Li-ion conductivity sulfide material with controlled LiX ratio and heat treatment | |

| CN104919628B | 2014 | Sulfide | 159 | CN, US, EP, JP, KR, WO, DE | Solid-state battery with sulfide electrolyte and metal interaction in anode to enhance output | |

| CN110537270B | 2018 | Sulfide | 163 | CN, US, JP, WO | All-solid-state battery with LiX-Li2S-P2S5 electrolyte and specific density to prevent conductive material不均 | |

| CN110391413B | 2019 | Sulfide | 159 | CN, US, EP, JP, KR, DE | Manufacturing method with initial charging to 4.35-4.55 V for alloy-based anode amorphousization | |

| LG Group | CN110114916B | 2018 | Polymer, Oxide | 73 | CN, US, EP, JP, KR, WO, DE, ES, HU | Electrode with 3D fibrous carbon structure for improved electronic and ionic conductivity |

| JP7282917B2 | 2020 | Polymer, Sulfide | 51 | CN, US, EP, JP, KR | Protective film on electrolyte surface using polyvinylidene carbonate to prevent reduction | |

| CN114269686B | 2021 | Sulfide | 69 | CN, US, EP, JP, KR, WO | Halogen- and germanium-free sulfide electrolyte via mixture heat treatment | |

| CN118613941A | 2023 | Polymer, Oxide | 26 | CN, EP, KR, WO | Composite solid electrolyte with polymer and ceramic for enhanced ion conductivity via UV curing | |

| Institute of Physics, Chinese Academy of Sciences | CN106684437B | 2017 | Sulfide, Oxide | 5 | CN | LixAlySzO2-z material combining oxide and sulfide advantages for high conductivity and stability |

| CN110120546B | 2018 | Polymer | 5 | CN | In-situ composite polymer electrolyte with fluoride coating for improved conductivity and interface stability | |

| CN115189012A | 2021 | Polymer, Sulfide | 86 | CN | Interdigitated solid-state battery cell with increased electrode-electrolyte contact area | |

| CN115000501A | 2022 | Sulfide | 52 | CN | New solid electrolyte Li2ADX4 with low ion migration barrier and high conductivity | |

| CN118367204A | 2024 | Sulfide | 62 | CN | Solid electrolyte Li8-xAX6-xClx with frustrated lattice for high ion conductivity up to 102 mS/cm |

Toyota Motor Corporation, the leader in solid-state electrolyte patents, has focused extensively on sulfide electrolytes since the 1990s. Key patents like CN102696141B disclose methods to minimize H2S production in sulfide materials, while CN103650231B highlights compositions with high Li-ion conductivity exceeding 1×10^{-4} S/cm. These innovations address critical challenges in solid state batteries, such as safety and performance. The LG Group has diversified across polymer, oxide, and sulfide branches, with patents like CN110114916B introducing 3D electrode structures for better conductivity and CN118613941A detailing composite electrolytes for enhanced ion transport. The Institute of Physics, Chinese Academy of Sciences, has made significant strides with patents like CN106684437B, which combines oxide and sulfide benefits, and CN118367204A, proposing new materials with ultra-high conductivity. These contributions underscore the global effort to overcome barriers in solid state battery technology, with mathematical models like the ion transport equation: $$ J = -D \frac{\partial C}{\partial x} + \frac{zF}{RT} D C \frac{\partial \phi}{\partial x} $$ where $J$ is the ion flux, $D$ is the diffusion coefficient, $C$ is the concentration, $z$ is the charge number, $F$ is Faraday’s constant, $R$ is the gas constant, $T$ is temperature, and $\phi$ is the electric potential. This equation highlights the complex dynamics involved in optimizing solid-state electrolytes for reliable solid state batteries.

Strategies and Recommendations for High-Quality Development

Based on the patent analysis, solid state batteries represent a cutting-edge technology attracting significant investment and attention from market players. With strong policy support and sustained R&D efforts, the industrialization of solid state batteries is expected to accelerate. We propose the following strategies to foster high-quality development in this sector.

First, after long-term accumulation, solid state batteries are now experiencing rapid advancement. Japan, with its early start and continuous technological development, led in patent applications until 2011. However, driven by the boom in China’s new energy vehicle industry, China has emerged as a key technology source, surpassing Japan in application volume by 2023. The core technologies of solid state batteries focus on the R&D of three solid-state electrolyte types: oxide, sulfide, and polymer. China leads in polymer branch applications, demonstrating deep expertise and market布局. In oxides, China and Japan are neck-and-neck, indicating intense competition. For sulfides, Japan maintains dominance due to early investments. Overall, the global competition in solid state battery technology shows China and Japan excelling in different branches. As worldwide attention and investment continue, this rivalry will intensify, further driving technological progress and industrialization. Chinese enterprises should capitalize on this by increasing R&D in solid state batteries, leveraging domestic supply chains and market scale to achieve breakthroughs.

Second, Chinese firms must intensify efforts in solid state battery technology R&D and patent布局, with particular emphasis on overseas patent strategies. While Japanese companies like Toyota lead in sulfide electrolytes, they do not hold overwhelming advantages in polymer and oxide branches. The development of all-solid-state batteries is a long-term race, with small-scale production anticipated by 2027-2030. Chinese companies should adopt a long-term perspective, boost R&D investment, and utilize China’s complete industry chain and vast market to accelerate technological leaps. Additionally, analysis of key applicants reveals that Chinese innovators’ patent布局 is primarily domestic, with few patent families and insufficient overseas presence. In contrast, international competitors like Toyota, Panasonic, and LG have widely布局 patents abroad. This gap could hinder Chinese products in export markets, so it is crucial to monitor competitor patent activities and expedite overseas布局 to enhance global competitiveness and safeguard market share.

Third, strengthening technical collaborations is essential for mutual benefit. Currently, universities face challenges in translating research into commercial outcomes, but some institutions, such as the Institute of Physics (Chinese Academy of Sciences) and Central South University, show strong potential in solid-state electrolyte patents. Meanwhile, automakers like BYD have heavily布局 polymer electrolytes, aligning with existing lithium-ion battery industrial systems. To integrate resources and improve R&D efficiency, China has established the “China All-Solid-State Battery Industry-University-Research Collaboration Platform,” bringing together research bodies, vehicle manufacturers, and battery producers to drive innovation and industrialization in all-solid-state batteries. Through synergy, this platform can address key issues in solid state battery technology, accelerating breakthroughs and commercialization. Such collaborations are vital for overcoming technical barriers and achieving high-quality development in the solid state battery industry.

Conclusion

Through in-depth mining of patents in the solid-state electrolyte field, we have clarified the technological layout differences among China, the U.S., Japan, and South Korea. China, the U.S., and South Korea focus primarily on polymer solid-state electrolytes, while Japan emphasizes sulfide solid-state electrolytes. Analysis of global key applicants shows that the top ten lack Chinese innovators, with Toyota, Panasonic, and LG Group leading. By identifying R&D-intensive research institutions, we found that Central South University, the Institute of Physics (Chinese Academy of Sciences), and Harbin Institute of Technology are among the strong domestic players. This patent data analysis guides Chinese enterprises in technology R&D and patent布局 directions. Solid state batteries are poised to revolutionize energy storage, and with strategic efforts, China can enhance its position in this critical field, contributing to global sustainable development. The ongoing innovations in solid state battery technologies will continue to shape the future of energy, making this an exciting area for further exploration and investment.