When I decided to embark on the entrepreneurial path, I was already in my fifties. At that time, I held a prestigious position as a chief engineer in the new energy vehicle sector, with a comfortable salary and benefits. Diving into startup life was met with skepticism from family and friends, but I felt a compelling drive: if I didn’t pursue this, I would regret it for the rest of my life. My goal was clear—to build a company that could go public. In 2016, I took on a new role as the founder and leader of a startup focused on solid-state battery technology.

Our company, established eight years ago, has completed multiple funding rounds, attracting investments from various automotive and industry players. Today, its valuation exceeds significant figures, reflecting the growing interest in solid-state batteries. In the power battery arena, solid-state batteries are often hailed as the “ultimate battery” due to their potential to balance energy density, safety, and cost. Research reports suggest that semi-solid and solid-state batteries could become a dominant trend, with 2024 marking the beginning of their adoption in vehicles. Moreover, solid-state batteries have gained policy support, with substantial government funding earmarked for their development, involving key industry participants.

We have filed over 500 patents and are involved in several national key R&D projects, spanning energy storage and automotive fields. In the solid-state battery race, from established liquid battery giants to startups like ours, everyone aims to replicate past successes in the liquid battery domain. Can we rise with this trend? The journey has been both challenging and enlightening.

In 2015, while still in my previous role, I was deeply involved in researching power battery technology pathways. I frequently collaborated with academic peers, and our shared interest in solid-state batteries sparked the idea of entrepreneurship. By late 2015, an investor approached me with an offer to fund a startup, which, though it didn’t materialize, highlighted the capital market’s enthusiasm. In 2016, I co-founded the company with colleagues, dedicating ourselves to the R&D of solid-state lithium batteries.

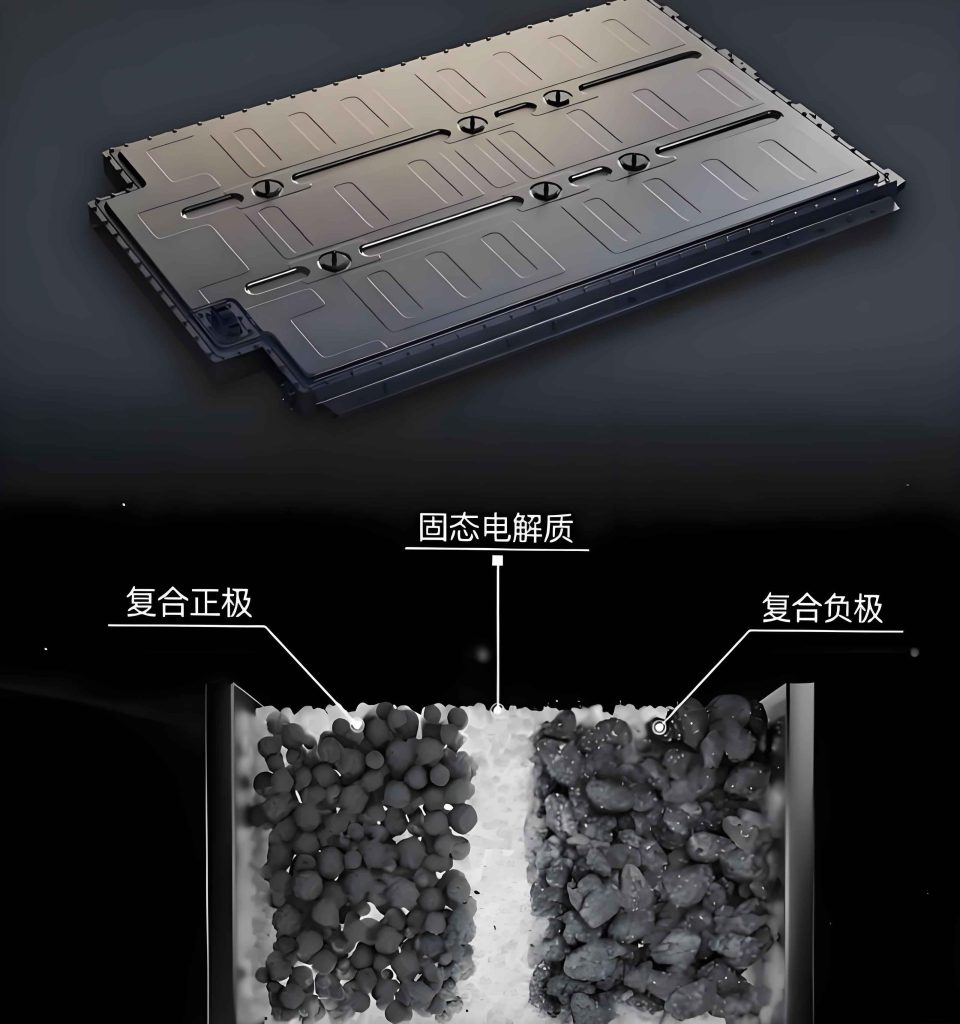

The initial challenge was defining the technical roadmap for solid-state batteries. Based on electrolyte materials, there are three main pathways: polymer, sulfide, and oxide. Each has its pros and cons. Polymers are cost-effective and easy to process but have low ionic conductivity. Sulfides offer high conductivity but are difficult and expensive to manufacture. In China, the oxide route is more prevalent, leading to a “gray zone” between liquid and all-solid-state batteries: semi-solid batteries. This involves reducing electrolyte content gradually, and we adopted an in-situ solidification approach, where part of the liquid transforms into solid, ensuring good electrode-electrolyte contact. This is the core of hybrid solid-liquid batteries.

At first, the industry viewed semi-solid batteries as a transitional product unlikely to achieve mass production. However, I believed that the semi-solid route was the optimal short-term solution for commercialization. It took nearly two years of trial and error to confirm this path in 2018. The development cycle for solid-state batteries is lengthy. Typically, cell R&D takes about two years, followed by integration with automakers, which can take 18 months to three years for validation and mass production. Overall, from inception to commercial deployment, it might take three to five years.

To sustain the company during this period, we explored various applications, such as batteries for mobile phones and Bluetooth earphones. However, after engaging with major consumer electronics brands, we realized the market was highly concentrated. We eventually streamlined our focus to solid-state power batteries, energy storage batteries, and small power battery cells, serving sectors like new energy vehicles and grid-scale storage. We now operate multiple production bases, and as output increases, revenue is expected to double this year.

As the founder, guiding the company from 0 to 1 and toward scaling, I’ve learned that organizational strength is crucial. Making rational decisions, minimizing execution deviations, and maximizing efficiency are continuous improvements. The transition to mass production presented significant hurdles.

In early 2021, a major automotive partner announced plans to incorporate a 150 kWh semi-solid battery with an energy density of 360 Wh/kg, targeting a 1000 km range. This brought solid-state batteries into the spotlight, and our company gained recognition. The collaboration was serendipitous; the automaker needed high-energy-density batteries for extended range, and solid-state batteries offered a solution beyond the 300 Wh/kg limit of liquid lithium batteries. After evaluations, we partnered in 2020, leading to the establishment of a production base that started construction in late 2021 and became operational in mid-2022.

Mass-producing solid-state batteries was daunting due to high costs and long testing cycles. We lacked experience in large-scale production, with new materials, teams, and equipment. I emphasized perseverance, learning, and dedication to the team. The automaker provided substantial support, with over 100 personnel onsite for joint development. By late 2022, we achieved the first automotive-grade solid-state power cell, and in 2023, we delivered 360 Wh/kg cells. The battery pack underwent testing and entered mass production in 2024, becoming available for use.

Currently, the battery pack is offered on a rental-only basis due to high costs, which are nearly double that of liquid batteries. This cost disparity is a key barrier to widespread adoption. However, we aim to reduce the cost gap to within 10% of ternary batteries this year. With increased production, particularly through cathode material cost reductions, semi-solid battery costs could align with liquid batteries. In the long run, all-solid-state batteries might be 10% to 20% cheaper than liquid ternary lithium batteries.

Scaling production is essential for cost reduction. Only with sufficient capacity can we negotiate better terms with suppliers and meet more automakers’ demands. I predict a tipping point around 2026, when more vehicles will adopt our semi-solid batteries. This year, we plan to partner with three automakers, but our priority remains fulfilling existing commitments. We must ramp up capacity gradually, ensuring product delivery before expanding further.

The solid-state battery landscape is evolving rapidly. Let’s delve into the technical aspects with formulas and tables. The energy density of a solid-state battery can be expressed as:

$$ \text{Energy Density} = \frac{E}{m} $$

where \( E \) is the energy stored and \( m \) is the mass. For solid-state batteries, this often exceeds 300 Wh/kg, a threshold limited by liquid electrolytes. The ionic conductivity \( \sigma \) of solid electrolytes is critical, given by:

$$ \sigma = n e \mu $$

with \( n \) as charge carrier concentration, \( e \) as electron charge, and \( \mu \) as mobility. Oxide-based electrolytes, common in our approach, balance conductivity and stability.

To compare technical routes, here’s a table summarizing key characteristics:

| Electrolyte Type | Advantages | Disadvantages | Conductivity (S/cm) |

|---|---|---|---|

| Polymer | Low cost, easy processing | Low ionic conductivity | ~10⁻⁵ |

| Sulfide | High conductivity | Expensive, difficult to manufacture | ~10⁻² |

| Oxide | Good balance, stable | Moderate conductivity | ~10⁻⁴ |

Our in-situ solidification process enhances interface contact, reducing impedance. The reaction kinetics can be modeled using:

$$ I = \frac{V}{R + R_{ct}} $$

where \( I \) is current, \( V \) voltage, \( R \) ohmic resistance, and \( R_{ct} \) charge transfer resistance. Solid-state batteries minimize \( R_{ct} \) through intimate interfaces.

Cost analysis is vital for adoption. The total cost \( C \) of a solid-state battery includes material, manufacturing, and R&D expenses:

$$ C = C_m + C_p + C_r $$

Initially, \( C_m \) is high due to novel materials like solid electrolytes. With scale, learning curves reduce costs. A projected cost comparison table:

| Battery Type | Current Cost ($/kWh) | Projected 2026 Cost ($/kWh) |

|---|---|---|

| Liquid Lithium-ion | 120 | 100 |

| Semi-Solid | 240 | 130 |

| All-Solid-State | N/A | 110 |

We anticipate that by 2026, semi-solid batteries will be cost-competitive, driving broader use. The safety advantage of solid-state batteries, with reduced flammability, adds value, quantified by lower failure rates \( \lambda \):

$$ \lambda_{\text{solid}} < \lambda_{\text{liquid}} $$

Our R&D focuses on optimizing these parameters. For instance, we work on composite electrolytes to boost conductivity. The effective medium theory approximates conductivity in composites:

$$ \sigma_{\text{eff}} = \sigma_1 \phi_1 + \sigma_2 \phi_2 $$

where \( \phi \) are volume fractions of components.

In production, yield \( Y \) impacts cost. We aim for \( Y > 95\% \) through process control. The relationship is:

$$ C_p \propto \frac{1}{Y} $$

Our facilities incorporate automation to enhance yield. Currently, we’re ramping up capacity, with plans to exceed several gigawatt-hours annually by 2025.

Market adoption hinges on energy density improvements. The solid-state battery’s theoretical limit surpasses 500 Wh/kg, but practical cells achieve 360-400 Wh/kg. We use high-nickel cathodes and lithium metal anodes, with capacity \( Q \) given by:

$$ Q = nF $$

where \( n \) is moles of lithium and \( F \) is Faraday’s constant. Cell design involves stacking layers, with thickness \( t \) influencing energy density:

$$ \text{Volumetric Energy Density} = \frac{E}{V} \approx \frac{Q \cdot V_{\text{cell}}}{A \cdot t} $$

for area \( A \).

Collaboration with automakers requires extensive testing. We follow standards like cycle life \( N \):

$$ N = \frac{\Delta \text{Capacity}}{\text{Decay Rate}} $$

targeting over 1000 cycles with minimal degradation. Our semi-solid cells show less than 20% capacity loss after 1000 cycles, outperforming many liquid counterparts.

Looking ahead, government policies and environmental regulations will accelerate solid-state battery adoption. Carbon neutrality goals favor high-energy-density, safe batteries. We project that by 2030, solid-state batteries could capture 20% of the global battery market, driven by electric vehicles and energy storage.

In summary, the journey with solid-state battery technology has been transformative. From initial doubts to technical breakthroughs, we’ve navigated challenges in R&D and production. The solid-state battery offers a promising future, with potential to revolutionize energy storage. As we scale, cost reductions and performance enhancements will make solid-state batteries a mainstream choice. The path forward requires continued innovation, collaboration, and resilience—a journey I’m proud to lead.