As an observer and analyst in the electric vehicle (EV) industry, I have witnessed numerous technological shifts, but few have generated as much excitement and debate as the recent push toward solid-state batteries. In early 2024, the automotive world was abuzz with claims of breakthroughs in solid-state battery technology, particularly from Chinese EV makers like IM Motors, GAC, and NIO. This surge in interest raises a critical question: are we on the cusp of a genuine revolution, or is this merely another marketing ploy? In this article, I will delve into the intricacies of solid-state batteries, examining their promises, the current state of development, and the challenges that lie ahead. My goal is to provide a comprehensive overview, using tables and formulas to clarify key concepts, while emphasizing the transformative potential of solid-state batteries for the future of transportation.

The narrative began in April 2024, when IM Motors launched its L6 model, touting it as the first production vehicle equipped with a “first-generation light-year solid-state battery.” This announcement ignited a flurry of discussions, with many hailing it as a milestone. However, skepticism quickly followed, as industry experts pointed out that what is being marketed as a solid-state battery is often a semi-solid-state variant. This distinction is crucial, as it underscores the gap between current offerings and the ultimate goal of all-solid-state batteries. To understand why, we must first explore what sets solid-state batteries apart from conventional lithium-ion batteries.

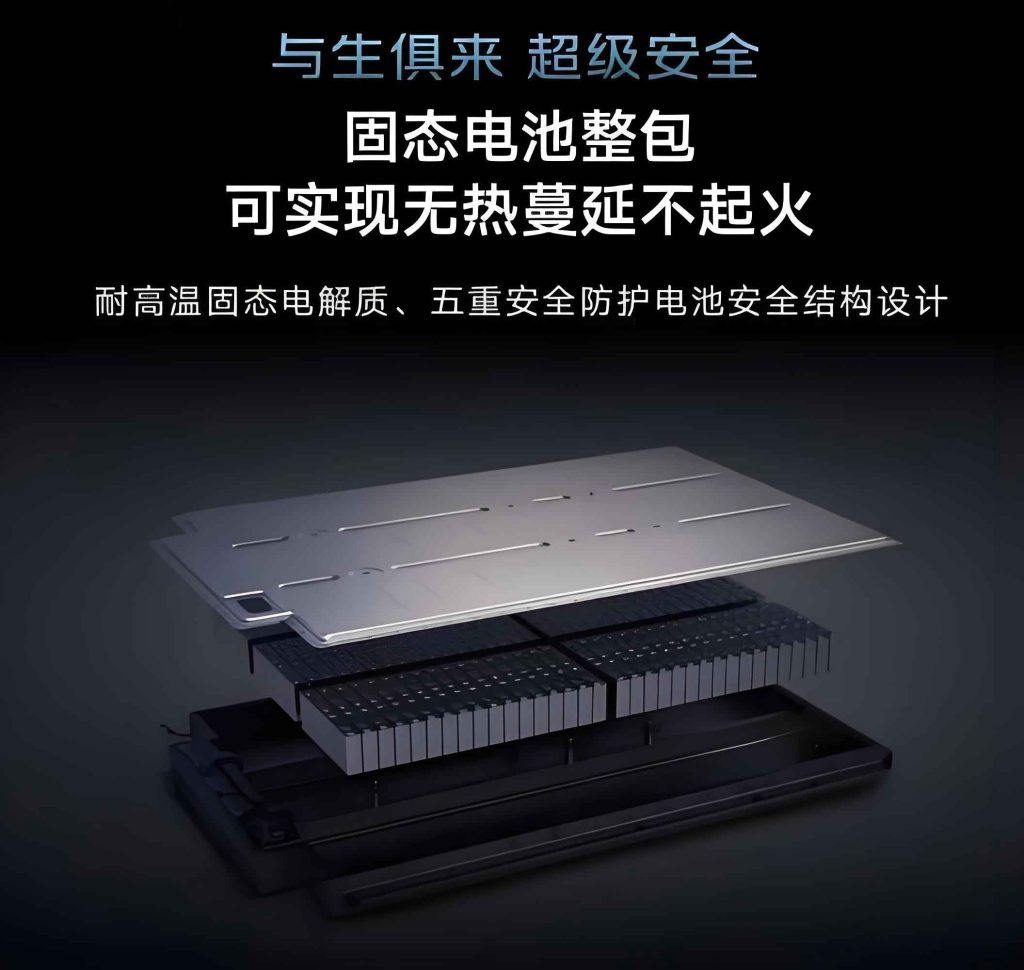

Traditional lithium-ion batteries, which power most EVs today, consist of a cathode, an anode, a separator, a liquid electrolyte, and a structural casing. The liquid electrolyte facilitates ion movement between electrodes but poses significant risks, such as thermal runaway leading to fires or explosions. In contrast, a true solid-state battery replaces the liquid electrolyte with a solid electrolyte, eliminating flammable components. This fundamental change brings three primary advantages: enhanced safety, higher energy density, and simplified packaging. Let’s break down each of these with technical details.

First, safety: solid-state batteries significantly reduce the risk of combustion. In liquid lithium-ion batteries, abnormal conditions like overcharging or internal shorts can cause the electrolyte to overheat, potentially triggering fires. The solid electrolyte in solid-state batteries is non-flammable, making them inherently safer. This can be expressed through a risk reduction factor. If we denote the probability of thermal runaway in liquid batteries as $$ P_{liquid} $$, and in solid-state batteries as $$ P_{solid} $$, the improvement can be modeled as $$ \Delta P = P_{liquid} – P_{solid} $$, where $$ \Delta P $$ is substantially positive due to the absence of volatile liquids.

Second, energy density: solid-state batteries promise dramatic increases in energy storage per unit mass or volume. This stems from several factors. The solid electrolyte eliminates the need for a separator and liquid electrolyte, which together occupy about 40% of the volume and 25% of the mass in traditional batteries. Additionally, the lack of leakage issues allows for simpler cooling systems and lighter casings. Moreover, solid-state batteries can operate at higher voltages, often above 5 V, enabling the use of advanced electrode materials. The energy density $$ E $$ can be calculated as $$ E = \frac{Q}{m} $$ for gravimetric energy density (Wh/kg) or $$ E_v = \frac{Q}{V} $$ for volumetric energy density (Wh/L), where $$ Q $$ is the energy capacity, $$ m $$ is the mass, and $$ V $$ is the volume. For solid-state batteries, both $$ E $$ and $$ E_v $$ are projected to be significantly higher than those of liquid counterparts.

Third, packaging simplification: without liquid components, solid-state batteries can use series connections within cells more efficiently, reducing the complexity of battery modules. This leads to a more compact design, with volumetric energy density potentially increasing by over 70% compared to liquid lithium-ion batteries. The relationship can be summarized as $$ V_{solid} = k \cdot V_{liquid} $$, where $$ k < 1 $$ represents the volume reduction factor, often around 0.7 or lower.

To illustrate these differences, here is a comparative table:

| Feature | Traditional Liquid Lithium-ion Battery | Semi-Solid-State Battery | All-Solid-State Battery |

|---|---|---|---|

| Electrolyte Type | Liquid organic electrolyte | Mixed solid-liquid electrolyte (liquid content >0%) | Solid electrolyte only (liquid content = 0%) |

| Safety Risk | High (flammable electrolyte) | Moderate (reduced flammability) | Low (non-flammable) |

| Gravimetric Energy Density (Wh/kg) | ~250-300 | ~300-400 | >400 (projected) |

| Volumetric Energy Density (Wh/L) | ~600-700 | ~700-900 | >1000 (projected) |

| Packaging Complexity | High (requires cooling systems, leak-proofing) | Medium (simplified cooling) | Low (minimal cooling, series cell structures) |

| Current Status | Mass-produced | Initial production (e.g., IM L6) | R&D and pilot stages |

The debate over semi-solid versus all-solid-state batteries is central to understanding the current landscape. A semi-solid-state battery still contains some liquid electrolyte, albeit in reduced amounts. Only when the liquid content reaches zero can it be called a true all-solid-state battery. This is not just semantics; it has practical implications for performance and safety. For instance, the solid-state battery in the IM L6, supplied by Qing Tao Technology, is part of a three-generation plan, with only the third generation—still in development—being fully solid-state. This highlights the incremental nature of progress in solid-state battery technology.

From an industrial perspective, semi-solid-state batteries offer a pragmatic compromise. They leverage existing lithium-ion production lines, reducing costs and accelerating adoption. The transition to all-solid-state batteries requires new manufacturing processes, such as solid electrolyte fabrication and electrode integration, which are still maturing. The cost reduction curve for solid-state batteries can be modeled as $$ C(t) = C_0 \cdot e^{-\alpha t} $$, where $$ C_0 $$ is the initial cost, $$ \alpha $$ is the learning rate, and $$ t $$ is time. Scaling up production is essential to drive down $$ C(t) $$, and semi-solid versions serve as a stepping stone.

The race for solid-state battery supremacy is heating up globally. Shortly after IM’s announcement, GAC revealed plans to complete all-solid-state battery development by 2026, deploying it in its Hyper model with an energy density exceeding 400 Wh/kg. This would represent a 50% boost in both volumetric and gravimetric energy density, enabling ranges over 1000 km. Similarly, Nissan announced in April 2024 that it will start all-solid-state battery production in March 2025, targeting mass production by 2028 with energy densities doubled from current levels. NIO has also been a pioneer, testing a 150 kWh semi-solid-state battery in late 2023 that achieved a 1000 km range in real-world driving. These developments underscore the intense competition and investment flowing into solid-state battery research.

To quantify the growth trajectory, let’s consider market forecasts. According to some securities analyses, the period from 2026 to 2030 is expected to be the scaling window for all-solid-state batteries. Demand for solid-state batteries could surpass 100 GWh by 2027 and reach 460 GWh by 2030. This growth can be expressed using a compound annual growth rate (CAGR) formula: $$ \text{CAGR} = \left( \frac{V_f}{V_i} \right)^{\frac{1}{n}} – 1 $$, where $$ V_i $$ is the initial demand, $$ V_f $$ is the future demand, and $$ n $$ is the number of years. Assuming $$ V_i $$ near zero now, the CAGR for solid-state batteries is projected to be exceptionally high, driven by EV adoption and technological advances.

The advantages of solid-state batteries extend beyond EVs to other applications like grid storage and portable electronics, but the automotive sector is the primary catalyst. The push for longer range, faster charging, and enhanced safety aligns perfectly with solid-state battery capabilities. For example, the “quasi-900 V ultra-fast charging” claimed for the IM L6’s battery highlights how solid-state batteries can support higher voltage architectures, reducing charging times. The charging power $$ P $$ is given by $$ P = V \times I $$, where $$ V $$ is voltage and $$ I $$ is current. With solid-state batteries enabling higher $$ V $$ without degradation, charging efficiency improves significantly.

However, challenges remain. The solid electrolyte materials, such as sulfides, oxides, or polymers, face issues like low ionic conductivity at room temperature or interfacial instability with electrodes. Research is focused on optimizing these materials. The ionic conductivity $$ \sigma $$ can be described by the Arrhenius equation: $$ \sigma = A e^{-\frac{E_a}{kT}} $$, where $$ A $$ is a pre-exponential factor, $$ E_a $$ is activation energy, $$ k $$ is Boltzmann’s constant, and $$ T $$ is temperature. For solid-state batteries, reducing $$ E_a $$ is key to achieving high $$ \sigma $$ at practical temperatures.

Another hurdle is durability. Solid-state batteries must withstand numerous charge-discharge cycles without performance loss. The cycle life $$ N $$ can be related to capacity retention $$ C_r $$ through empirical models, such as $$ C_r(N) = C_0 (1 – \beta N) $$, where $$ C_0 $$ is initial capacity and $$ \beta $$ is a degradation rate. Solid-state batteries aim for lower $$ \beta $$ values than liquid batteries.

To illustrate the technological progression, here is a timeline table for solid-state battery development:

| Year | Milestone | Key Players | Energy Density (Wh/kg) | Type |

|---|---|---|---|---|

| 2023 | NIO tests 150 kWh semi-solid-state battery | NIO, WeLion | ~360 | Semi-solid |

| 2024 | IM L6 launches with “first-gen” solid-state battery | IM Motors, Qing Tao | ~300-350 | Semi-solid |

| 2025 | Nissan starts pilot production | Nissan | ~400 (projected) | All-solid |

| 2026 | GAC targets all-solid-state battery deployment | GAC | >400 | All-solid |

| 2028 | Mass production goals for all-solid-state | Multiple (Toyota, BMW, etc.) | >500 | All-solid |

| 2030 | Market scale expected to exceed 460 GWh | Global industry | >600 | All-solid |

The economic implications are profound. As solid-state batteries become mainstream, they could reshape the entire EV supply chain. Battery costs, which currently account for a significant portion of EV prices, may decline due to material savings and simpler manufacturing. The total cost of ownership (TCO) for EVs with solid-state batteries could be lower than for those with liquid batteries, calculated as $$ \text{TCO} = C_{\text{battery}} + C_{\text{charging}} + C_{\text{maintenance}} $$. With higher energy density, $$ C_{\text{battery}} $$ per kWh drops, and longer lifespan reduces $$ C_{\text{maintenance}} $$.

Environmental benefits also accrue. Solid-state batteries often use less toxic materials and have better recyclability. The life-cycle assessment (LCA) impact can be modeled as $$ \text{LCA} = \int_0^L E(t) \, dt $$, where $$ E(t) $$ is the environmental burden over time $$ t $$, and $$ L $$ is the battery life. Solid-state batteries tend to have lower $$ E(t) $$ due to reduced resource extraction and waste.

In my view, the journey toward solid-state batteries is not without hype, but the underlying technological strides are real. The transition from liquid to solid electrolytes represents a paradigm shift akin to moving from internal combustion engines to electric motors. While semi-solid-state batteries are an interim solution, they pave the way for the ultimate goal: all-solid-state batteries that deliver on the full promise of safety, performance, and sustainability.

Looking ahead, collaboration between automakers, battery producers, and research institutions will be crucial. Standardization of materials and processes will accelerate adoption. Governments may also play a role through incentives for solid-state battery development, similar to those for renewable energy. The global solid-state battery market is poised for explosive growth, and I believe it will be a cornerstone of the next generation of electric mobility.

To summarize, solid-state batteries are more than just a marketing buzzword; they are a transformative technology with the potential to overcome the limitations of current lithium-ion batteries. From enhanced safety to higher energy densities, the advantages are compelling. As the industry navigates the challenges of scaling up all-solid-state versions, the progress in semi-solid-state batteries offers a glimpse into a future where EVs can travel farther, charge faster, and operate more safely. The solid-state battery revolution is indeed underway, and its impact will resonate across the automotive landscape for decades to come.

In conclusion, as we witness this exciting era of innovation, it is clear that solid-state batteries hold the key to unlocking the full potential of electric vehicles. The road ahead may be fraught with technical hurdles, but the collective efforts of the industry suggest that a future powered by solid-state batteries is not just a dream—it is an imminent reality. I am optimistic that with continued research and investment, solid-state batteries will soon become the standard, driving us toward a cleaner, safer, and more efficient transportation system.